Xcel Energy 2009 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2009 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

ASC 740 Income Taxes also requires that only tax benefits that meet the ‘‘more likely than not’’ recognition threshold

can be recognized or continue to be recognized. The change in the unrecognized tax benefits needs to be reasonably

estimated based on evaluation of the nature of uncertainty, the nature of event that could cause the change and an

estimated range of reasonably possible changes. At any period end, and as new developments occur, management will

use prudent business judgment to unrecognize appropriate amounts of tax benefits. Unrecognized tax benefits can be

recognized as issues are favorably resolved and loss exposures decline.

As disputes with the IRS and state tax authorities are resolved over time, we may need to adjust our unrecognized tax

benefits and interest accruals to the updated estimates needed to satisfy tax and interest obligations for the related

issues. These adjustments may be favorable or unfavorable, increasing or decreasing earnings.

See Note 8 for further details regarding income taxes.

Employee Benefits

Xcel Energy’s pension costs are based on an actuarial calculation that includes a number of key assumptions, most

notably the annual return level that pension investment assets will earn in the future and the interest rate used to

discount future pension benefit payments to a present value obligation for financial reporting. In addition, the actuarial

calculation uses an asset-smoothing methodology to reduce the volatility of varying investment performance over time.

Note 11 to the consolidated financial statements discusses the rate of return and discount rate used in the calculation of

pension costs and obligations in the accompanying financial statements.

Pension costs and funding requirements are expected to increase in the next few years as a result of significantly

lower-than-expected investment returns in 2008. While investment returns exceeded the assumed levels from

2004-2006, and during 2009, investment returns in 2007 and 2008 were below the assumed levels. The investment

gains or losses resulting from the difference between the expected pension returns and actual returns earned are deferred

in the year the difference arises and are recognized over the expected average remaining years of service for active

employees. Based on current assumptions and the recognition of past investment gains and losses, Xcel Energy currently

projects that the pension costs recognized for financial reporting purposes will increase from income of $3.0 million in

2008 and an expense of $12.9 million in 2009 to expense of $36 million in 2010 and expense of $110 million in

2011. The potential increase in the 2011 expense is due to expense recognition based on cash funding and expected

cash contributions of $55 million in 2011 at NSP-Minnesota compared to no contributions made during 2008 through

2010.

Xcel Energy set the discount rate used to value the Dec. 31, 2009 pension and postretirement health care obligations at

6 percent, which is a 75 basis point decrease from Dec. 31, 2008. Xcel Energy uses multiple reference points in

determining the discount rate, including Citigroup Pension Liability Discount Curve, the Citigroup Above Median

Curve and bond matching studies. At Dec. 31, 2009, the above reference points supported the selected rate. In addition

to the reference points utilized above, Xcel Energy also reviews general survey data provided by our actuaries to assess

the reasonableness of the discount rate selected.

The Pension Protection Act changed the minimum funding requirements for defined benefit pension plans beginning in

2008. Xcel Energy accelerated its planned 2010 contribution of $100 million based on available liquidity, bringing its

total pension contributions to $200 million during 2009. Xcel Energy currently projects no additional funding for 2010

and cash funding of $100 million to $150 million in 2011. For future years, we anticipate contributions will be made

to avoid benefit restrictions and at-risk status.

These expected contributions are summarized in Note 11 to the consolidated financial statements. These amounts are

estimates and may change based on actual market performance, changes in interest rates and any changes in

governmental regulations. Therefore, additional contributions could be required in the future. However, all pension

costs are expected to be recoverable in rates.

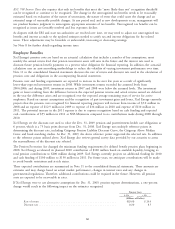

If Xcel Energy were to use alternative assumptions for Dec. 31, 2009, pension expense determinations, a one-percent

change would result in the following impact on the estimates recognized:

Pension Costs

1% 1%

(Millions of Dollars)

Rate of return ............................................. $(20.0) $ 20.0

Discount rate .............................................. (6.0) 8.5

66