Xcel Energy 2009 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2009 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

ASC 820 Fair Value Measurements establishes a hierarchal framework for disclosing the observability of the inputs

utilized in measuring fair value. The three levels defined by the hierarchy and examples of each level are as follows:

Level 1 — Quoted prices are available in active markets for identical assets as of the reporting date. The types of

assets included in Level 1 are highly liquid and actively traded instruments with quoted prices, such as common

stocks listed by the New York Stock Exchange.

Level 2 — Pricing inputs are other than quoted prices in active markets, but are either directly or indirectly

observable as of the reporting date. The types of assets included in Level 2 are typically either comparable to

actively traded securities or contracts or priced with models using highly observable inputs, such as corporate bonds

with pricing based on market interest rate curves and recent trades of similarly rated securities.

Level 3 — Significant inputs to pricing have little or no observability as of the reporting date. The types of assets

included in Level 3 are those with inputs requiring significant management judgment or estimation, such as asset

and mortgage backed securities, for which subjective risk-based adjustments to estimated yield and forecasted

prepayments are significant inputs.

Pension Benefits

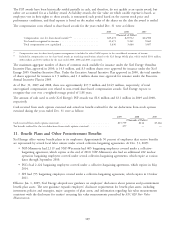

Xcel Energy has several noncontributory, defined benefit pension plans that cover almost all employees. Benefits are

based on a combination of years of service, the employee’s average pay and social security benefits. Xcel Energy’s policy

is to fully fund the actuarially determined pension costs recognized for ratemaking and financial reporting purposes,

subject to the limitations of applicable employee benefit and tax laws, into an external trust over time.

Xcel Energy bases its investment-return assumption on expected long-term performance for each of the investment types

included in its pension asset portfolio. Xcel Energy considers the actual historical returns achieved by its asset portfolio

over the past 20-year or longer period, as well as the long-term return levels projected and recommended by investment

experts. The historical weighted average annual return for the past 20 years for the Xcel Energy portfolio of pension

investments is 8.98 percent, which is greater than the current assumption level. The pension cost determination assumes

a forecasted mix of investment types over the long term. Investment returns in 2009 were above the assumed level of

8.50 percent while returns in 2008 and 2007 were below the assumed level of 8.75 percent. Xcel Energy continually

reviews its pension assumptions. In 2010, Xcel Energy will use an investment-return assumption of 7.79 percent.

The assets are invested in a portfolio according to Xcel Energy’s return, liquidity and diversification objectives to

provide a source of funding for plan obligations and minimize the necessity of contributions to the plan, within

appropriate levels of risk. The principal mechanism for achieving these objectives is the allocation of assets to selected

asset classes, given the long-term risk, return, and liquidity characteristics of each particular asset class. There were no

significant concentrations of risk in any particular industry, index, or entity, however, a higher weighting in equity

investments can increase the volatility in the return levels achieved by pension assets in any year.

The following table presents the target pension asset allocations for 2009 and 2008:

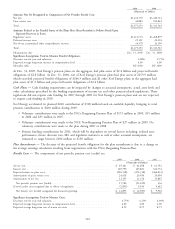

2009 2008

Domestic and international equity securities ........................... 24% 52%

Long duration fixed income securities ............................... 34 —

Short to intermediate fixed income securities .......................... 19 25

Alternative investments ........................................ 18 23

Cash ................................................... 5 —

Total ................................................. 100% 100%

In 2009, Xcel Energy engaged J.P. Morgan’s Pension Advisory Group to evaluate the allocation of the total assets in the

master pension trust, taking into consideration the funded status of each individual pension plan provided by Xcel

Energy. The investment strategy employed during 2009 is based on plan-specific investment recommendations that seek

to minimize potential investment and interest rate risk as a plan’s funded status increases over time. The investment

recommendations result in a greater percentage of short-to-intermediate term and long-duration fixed income securities

being allocated to specific plans having relatively higher funded status ratios, and a greater percentage of growth assets

being allocated to plans having relatively lower funded status ratios. The aggregate asset allocation presented in the table

above for the master pension trust results from the plan-specific strategies.

110