Shaw 2012 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2012 Shaw annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

|

|

Shaw Communications Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

August 31, 2012 and 2011

[all amounts in millions of Canadian dollars except share and per share amounts]

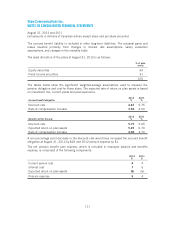

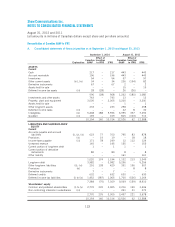

Credit risk

Accounts receivable in respect of Cable and Satellite divisions are not subject to any significant

concentrations of credit risk due to the Company’s large and diverse customer base. For the

Media division, a significant portion of sales are made to advertising agencies which results in

some concentration of credit risk. At August 31, 2012, approximately 58% (2011 – 58%) of

the $182 (2011 – $176) of advertising receivables is due from the ten largest accounts. The

largest amount due from an advertising agency is $20 (2011 – $20) which is approximately

11% (2011 – 12%) of advertising receivables. As at August 31, 2012, the Company had

accounts receivable of $433 (August 31, 2011 – $443; September 1, 2010 – $196), net of

the allowance for doubtful accounts of $28 (August 31, 2011 – $29; September 1, 2010 –

$19). The Company maintains an allowance for doubtful accounts for the estimated losses

resulting from the inability of its customers to make required payments. In determining the

allowance, the Company considers factors such as the number of days the subscriber account is

past due, whether or not the customer continues to receive service, the Company’s past

collection history and changes in business circumstances. As at August 31, 2012, $111

(August 31, 2011 – $121; September 1, 2010 – $79) of accounts receivable is considered to

be past due, defined as amounts outstanding past normal credit terms and conditions.

Uncollectible accounts receivable are charged against the allowance account based on the age

of the account and payment history. The Company believes that its allowance for doubtful

accounts is sufficient to reflect the related credit risk.

The Company mitigates the credit risk of advertising receivables by performing initial and

ongoing credit evaluations of advertising customers. Credit is extended and credit limits are

determined based on credit assessment criteria and credit quality. In addition, the Company

mitigates credit risk of subscriber receivables through advance billing and procedures to

downgrade or suspend services on accounts that have exceeded agreed credit terms.

Credit risks associated with cross-currency interest rate exchange agreements and US currency

contracts arise from the inability of counterparties to meet the terms of the contracts. In the

event of non-performance by the counterparties, the Company’s accounting loss would be

limited to the net amount that it would be entitled to receive under the contracts and

agreements. In order to minimize the risk of counterparty default under its swap agreements,

the Company assesses the creditworthiness of its swap counterparties. Currently 100% of the

total swap portfolio is held by a financial institution with Standard & Poor’s ratings ranging from

A+ to A-1.

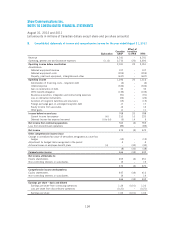

Liquidity risk

Liquidity risk is the risk that the Company will experience difficulty in meeting obligations

associated with financial liabilities. The Company manages its liquidity risk by monitoring cash

flow generated from operations, available borrowing capacity, and by managing the maturity

profiles of its long-term debt.

118