Sara Lee 2010 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2010 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

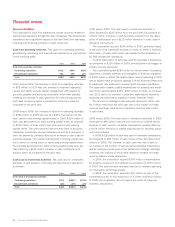

Self-Insurance Reserves The corporation purchases third-party

insurance for workers’ compensation, automobile and product and

general liability claims that exceed a certain level. The corporation

is responsible for the payment of claims under these insured limits,

and consulting actuaries are utilized to estimate the obligation

associated with incurred losses. Historical loss development factors

are utilized to project the future development of incurred losses,

and these amounts are adjusted based upon actual claim experi-

ence and settlements. Consulting actuaries make a significant

number of estimates and assumptions in determining the cost to

settle these claims and many of the factors used are outside the

control of the corporation. Accordingly, it is reasonably likely that

these assumptions and estimates may change and these changes

may impact future financial results.

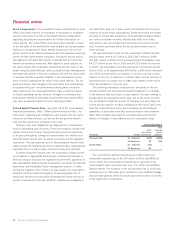

Income Taxes Deferred taxes are recognized for the future tax

effects of temporary differences between financial and income

tax reporting using tax rates in effect for the years in which the

differences are expected to reverse. Federal and state income

taxes are provided on that portion of foreign subsidiaries income

that is expected to be remitted to the U.S. and be taxable.

The corporation’s effective tax rate is based on pretax income,

statutory tax rates and tax planning opportunities available in the

various jurisdictions in which the corporation operates. There are

inherent uncertainties related to the interpretation of tax regulations

in the jurisdictions in which the corporation transacts business. We

establish reserves for income taxes when, despite the belief that

our tax positions are fully supportable, we believe that our position

may be challenged and possibly disallowed by various tax authorities.

The corporation’s recorded estimates of liability related to income

tax positions are based on management’s judgments made in con-

sultation with outside tax and legal counsel, where appropriate, and

are based upon the expected outcome of proceedings with world-

wide tax authorities in consideration of applicable tax statutes and

related interpretations and precedents. We also provide interest on

these reserves at the appropriate statutory interest rates and these

charges are also included in the corporation’s effective tax rate.

The ultimate liability incurred by the corporation may differ from its

estimates based on a number of factors, including the application

of relevant legal precedent, the corporation’s success in supporting

its filing positions with tax authorities, and changes to, or further

interpretations of, law.

The corporation’s tax returns are routinely audited by federal,

state, and foreign tax authorities. Reserves for uncertain tax posi-

tions represent a provision for the corporation’s best estimate of

taxes expected to be paid based upon all available evidence recog-

nizing that over time, as more information is known, these reserves

may require adjustment. Reserves are adjusted when (a) new infor-

mation indicates a different estimated reserve is appropriate; (b)

the corporation finalizes an examination with a tax authority, elimi-

nating uncertainty regarding tax positions taken; or (c) a tax authority

does not examine a tax year within a given statute of limitations,

also eliminating the uncertainty with regard to tax positions for a

specific tax period. The actual amounts settled with respect to these

examinations were the result of discussions and settlement negoti-

ations involving the interpretation of complex income tax laws in the

context of our fact patterns. Any adjustment to a tax reserve impacts

the corporation’s tax expense in the period in which the adjustment

is made.

As a global commercial enterprise, the corporation’s tax rate from

period to period can be affected by many factors. The most signifi-

cant of these factors are changes in tax legislation, the corporation’s

global mix of earnings, the tax characteristics of the corporation’s

income, the timing and recognition of goodwill impairments, acquisi-

tions and dispositions, adjustments to the corporation’s reserves

related to uncertain tax positions, changes in valuation allowances,

and the portion of the income of foreign subsidiaries that is expected

to be remitted to the U.S. and be taxable. It is reasonably possible

that the following items can have a material impact on income tax

expense, net income and liquidity in future periods:

•The spin off of the Hanesbrands business that was completed

in 2007 has resulted in an increase in the corporation’s effective

tax rate as the operations that were spun off had, historically, a

lower effective tax rate than the remainder of the business and gen-

erated a significant amount of operating cash flow. The elimination

of this cash flow has required the corporation to remit a greater

portion of the future foreign earnings to the U.S. than has historically

been the case and resulted in higher levels of tax expense and

cash taxes paid. The tax provision associated with the repatriation

of foreign earnings for both continuing and discontinued operations

in fiscal years 2010, 2009, and 2008 was $574 million, $58 mil-

lion, and $118 million, respectively. In 2010, the tax expense for

46 Sara Lee Corporation and Subsidiaries

Financial review