Sara Lee 2010 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2010 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

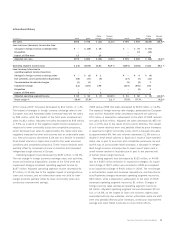

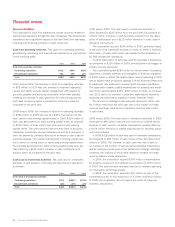

Sales Recognition and Incentives Sales are recognized when title

and risk of loss pass to the customer. Reserves for uncollectible

accounts are based upon historical collection statistics, current

customer information, and overall economic conditions. These

estimates are reviewed each quarter and adjusted based upon

actual experience. The reserves for uncollectible trade receivables

are disclosed and trade receivables due from customers that the

corporation considers highly leveraged are presented in Note 15 to

the Consolidated Financial Statements, titled “Financial Instruments

and Risk Management Interest Rate and Currency Swaps.” The

corporation has a significant number of individual accounts receiv-

able and a number of factors outside of the corporation’s control

that impact the collectibility of a receivable. It is reasonably likely

that actual collection experience will vary from the assumptions

and estimates made at the end of each accounting period.

The Notes to the Consolidated Financial Statements specify a

variety of sales incentives that the corporation offers to resellers

and consumers of its products. Measuring the cost of these incen-

tives requires, in many cases, estimating future customer utilization

and redemption rates. Historical data for similar transactions are

used in estimating the most likely cost of current incentive programs.

These estimates are reviewed each quarter and adjusted based

upon actual experience and other available information. The corpo-

ration has a significant number of trade incentive programs and a

number of factors outside of the corporation’s control impact the

ultimate cost of these programs. It is reasonably likely that actual

experience will vary from the assumptions and estimates made

at the end of each accounting period.

Inventory Valuation Inventory is carried on the balance sheet at

the lower of cost or market. Obsolete, damaged and excess inven-

tories are carried at net realizable value. Historical recovery rates,

current market conditions, future marketing and sales plans and

spoilage rates are key factors used by the corporation in assessing

the most likely net realizable value of obsolete, damaged and excess

inventory. These factors are evaluated at a point in time and there

are inherent uncertainties related to determining the recoverability

of inventory. It is reasonably likely that market factors and other

conditions underlying the valuation of inventory may change in

the future.

Impairment of Property Property is tested for recoverability

whenever events or changes in circumstances indicate that its

carrying value may not be recoverable. Such events include sig -

nificant adverse changes in the business climate, the impact of

significant customer losses, current period operating or cash flow

losses, forecasted continuing losses or a current expectation that

an asset group will be disposed of before the end of its useful life.

Recoverability of property is evaluated by a comparison of the carry-

ing amount of an asset or asset group to future net undiscounted

cash flows expected to be generated by the asset or asset group.

If these comparisons indicate that an asset is not recoverable, the

impairment loss recognized is the amount by which the carrying

amount of the asset exceeds the estimated fair value. When an

impairment loss is recognized for assets to be held and used, the

adjusted carrying amount of those assets is depreciated over its

remaining useful life. Restoration of a previously recognized impair-

ment loss is not allowed.

There are inherent uncertainties associated with these judgments

and estimates and it is reasonably likely that impairment charges

can change from period to period. Note 4 to the Consolidated

Financial Statements discloses the impairment charges recognized

by the corporation and the factors which caused these charges. It

is also reasonably likely that the sale of a business can result in

the recognition of an impairment that differs from that anticipated

prior to the closing date. Given the corporation’s ongoing efforts

to improve operating efficiency, it is reasonably likely that future

restructuring actions could result in decisions to dispose of other

assets before the end of their useful life and it is reasonably likely

that the impact of these decisions would result in impairment and

other related costs including employee severance that in the

aggregate would be significant.

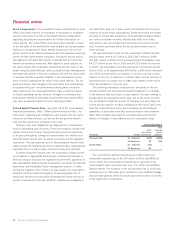

Trademarks and Other Identifiable Intangible Assets The primary

identifiable intangible assets of the corporation are trademarks

and customer relationships acquired in business combinations

and computer software. Identifiable intangibles with finite lives are

amortized and those with indefinite lives are not amortized. The

estimated useful life of an identifiable intangible asset to the cor-

poration is based upon a number of factors, including the effects

of demand, competition, expected changes in distribution channels

and the level of maintenance expenditures required to obtain future

cash flows. As of July 3, 2010, the net book value of trademarks

and other identifiable intangible assets was $504 million, of which

$450 million is being amortized. The anticipated amortization over

the next five years is $219 million.

44 Sara Lee Corporation and Subsidiaries

Financial review