Reebok 2011 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2011 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

|

|

adidas Group

2011 Annual Report

GROUP MANAGEMENT REPORT – OUR GROUP

63

2011

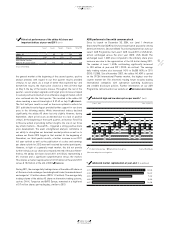

02.2 Global Sales Strategy Wholesale Strategy

Wholesale Strategy

The main strategic objective of the Wholesale channel is to deliver

profitable market share growth by becoming the leading sales

organisation in the sporting goods industry in terms of effectiveness

and efficiency. To realise this, Wholesale takes the go-to-market

strategies handed over by Global Brands and commercialises them

within a defined framework across various third-party retail channels.

Our most important third-party retail channels are sporting goods

chains, department stores, independent sporting goods retailer

buying groups, lifestyle retail chains and e-tailers. In this respect,

Wholesale strives to establish strong partnerships with the most

dynamic retailers in their respective channel of distribution by offering

best-in-class and tailored services. To achieve this, Wholesale has

established the following principles

DIAGRAM 01

:

– Amplify our brands at the point of sale (POS) in all relevant channels

– Build strong relationships with leading and most dynamic retailers

– Build a highly motivated and highly skilled sales team

– Implement an industry-leading sales toolkit to drive sell-out

– Deliver the benchmark in servicing retailers with world-class

efficiency

To reach our Route 2015 objectives, we have identified several focus

areas, built upon these principles.

Retail Space Management to amplify our brands at POS

Retail Space Management (RSM) comprises all business models

helping our Global Sales function to expand controlled space in retail.

Under the premise that the selling process is not finished until the

consumer has bought the product, Wholesale is cooperating with

retailers along the entire supply chain to bring best-in-class service

all the way through to the point of sale. By helping to increase profit-

ability per square metre for the Group’s retail partners as well as

improving product availability, we can achieve higher customer satis-

faction, thus driving share of retail shelf space.

The two predominant models to drive the success of RSM for the

adidas Group are Franchising and Never-out-of-stock (NOOS).

– Franchising: Mono-branded store franchising is one of the Group’s

prime growth opportunities, as it offers superior brand presentation

while limiting investment requirements and costs. Franchise stores

are financed and operated by franchise partners. The adidas Group

normally contributes to the costs for brand-specific fixtures and fittings

each store has to be equipped with. Furthermore, we support our

franchise partners with a comprehensive franchise concept, including

range propositions, merchandising, training concepts, and guidelines

for store building and store operations. This ensures that the quality of

the brand presentation and the service offered to the consumer are at

all times high and comparable to our own-retail stores.

− NOOS: The NOOS programme comprises a core range of basic

articles, mostly on an 18- to 24-month life cycle, that are selling

across all channels and markets. Overall, the NOOS replenishment

model secures high levels of product availability throughout the

season, allowing for quick adaptation to demand patterns. Retailers

have to provide dedicated retail space, co-invest in fixtures and

fittings and commit to a “first fill” representing about 25% of total

expected seasonal demand to participate in this programme. In

return, customers can profit from significantly reduced inventory risk

on these products. Most NOOS articles are on an end-to-end supply

chain, thus limiting the adidas Group’s inventory risk and increasing

availability of products sold at best price as we re-produce based on

customer demand.

Harmonisation and standardisation of processes to

exploit leverage

Wholesale is constantly working on further leveraging the size of our

Group and reducing complexity by implementing best operational

practices across our wholesale activities. The harmonisation and

standardisation particularly of back-end processes can help to further

reduce cost through simplified IT systems and processes.

Similarly, we are rolling out a trade terms policy globally that rewards

customer performance either by higher efficiency (e.g. in logistics),

cost savings or better sell-out support (e.g. by POS activation). As

part of this effort, we have established regular reporting, delivering

meaningful benchmarks that allow us to tightly control our third-party

retail support activities.

01 Wholesale strategic pillars

Amplify our brands at the

point of sale (POS) in all

relevant channels

Build strong relationships

with leading and most

dynamic retailers

Build a highly motivated

and highly skilled sales

team

Implement an industry-

leading sales toolkit to

drive sell-out

Deliver the benchmark

in servicing retailers with

world-class efficiency

To be the globally leading sales organisation

in the sporting goods industry