Reebok 2011 Annual Report Download - page 186

Download and view the complete annual report

Please find page 186 of the 2011 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

|

|

adidas Group

2011 Annual Report

CONSOLIDATED FINANCIAL STATEMENTS

04.8 Notes

182

2011

182

2011

04.8

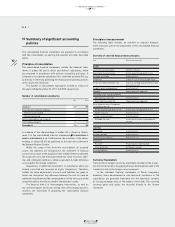

02 Summary of significant accounting

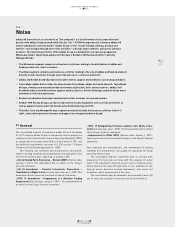

policies

The consolidated financial statements are prepared in accordance

with the consolidation, accounting and valuation principles described

below.

Principles of consolidation

The consolidated financial statements include the financial state-

ments of adidas AG and its direct and indirect subsidiaries, which

are prepared in accordance with uniform accounting principles. A

company is considered a subsidiary if it is controlled by adidas AG, e.g.

by directly or indirectly governing the financial and operating policies

of the respective enterprise.

The number of consolidated subsidiaries evolved as follows for

the years ending December 31, 2011 and 2010, respectively:

Number of consolidated subsidiaries

2011 2010

January 1 169 177

First-time consolidated companies: 6 1

Thereof: newly founded 4 1

Thereof: purchased 2 –

Deconsolidated/divested companies – (1)

Intercompany mergers (2) (8)

December 31 173 169

A schedule of the shareholdings of adidas AG is shown in Attach-

ment II to the consolidated financial statements

SEE SHAREHOLDINGS OF

ADIDAS AG, HERZOGENAURACH, P. 218

. Furthermore, the schedule of the share-

holdings of adidas AG will be published on the electronic platform of

the German Federal Gazette.

Within the scope of the first-time consolidation, all acquired

assets and liabilities are recognised in the statement of financial

position at fair value at the acquisition date. A debit difference between

the acquisition cost and the proportionate fair value of assets, liabil-

ities and contingent liabilities is shown as goodwill. A credit difference

is recorded in the income statement.

Acquisitions of additional investments in subsidiaries which are

already controlled are recorded as equity transactions. Therefore,

neither fair value adjustments of assets and liabilities nor gains or

losses are recognised. Any difference between the cost for such an

additional investment and the carrying amount of the net assets at the

acquisition date is directly recorded in shareholders’ equity.

The financial effects of intercompany transactions, as well as

any unrealised gains and losses arising from intercompany business

relations are eliminated in preparing the consolidated financial

statements.

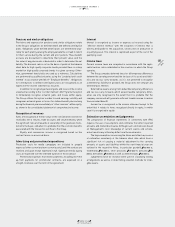

Principles of measurement

The following table includes an overview of selected measure-

ment principles used in the preparation of the consolidated financial

statements.

Overview of selected measurement principles

Item Measurement principle

Assets

Cash and cash equivalents Nominal amount

Short-term financial assets At fair value through profit or loss

Accounts receivable Amortised cost

Inventories Lower of cost or net realisable value

Assets classified as held for sale Lower of carrying amount and fair value

less costs to sell

Property, plant and equipment Amortised cost

Goodwill Impairment-only approach

Intangible assets (except goodwill):

With definite useful life Amortised cost

With indefinite useful life Impairment-only approach

Other financial assets (categories

according to IAS 39):

At fair value through profit or loss At fair value through profit or loss

Held to maturity Amortised cost

Loans and receivables Amortised cost

Available-for-sale At fair value in other comprehensive

income

Liabilities

Borrowings Amortised cost

Accounts payable Amortised cost

Other financial liabilities Amortised cost

Provisions:

Pensions Projected unit credit method

Other provisions Settlement amount

Accrued liabilities Amortised cost

Currency translation

Transactions in foreign currencies are initially recorded in the respec-

tive functional currency by applying the spot exchange rate valid at the

transaction date to the foreign currency amount.

In the individual financial statements of Group companies,

monetary items denominated in non-functional currencies of the

subsidiaries are generally translated into the functional currency

at closing exchange rates at the balance sheet date. The resulting

currency gains and losses are recorded directly in the income

statement.