Pep Boys 2006 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2006 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

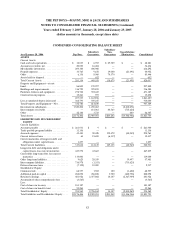

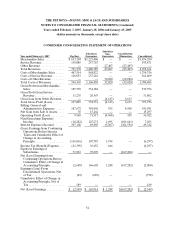

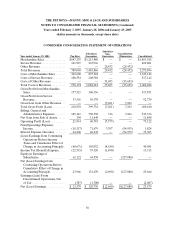

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 3, 2007, January 28, 2006 and January 29, 2005

(dollar amounts in thousands, except share data)

46

the interest rate under the agreement to LIBOR plus 1.75% (after June 1, 2005, the rate decreased to

LIBOR plus 1.50%, subject to 0.25% incremental increases as excess availability falls below $50,000). The

amendment also provided the flexibility, upon satisfaction of certain conditions, to release up to $99,000 of

reserved credit line availability required as of December 2, 2004 under the line of credit agreement to

support certain operating leases. This reserve was $73,912 on February 3, 2007. Finally, the amendment

extended the term of the agreement through December 2009. The weighted average interest rate on

borrowings under the line of credit agreement was 7.67 % and 6.2% at February 3, 2007 and January 28,

2006, respectively.

In the third quarter of fiscal 2004, the Company entered into a vendor financing program with an

availability of $20,000. Under this program, the Company’s factor makes accelerated and discounted

payments to its vendors and the Company, in turn, makes its regularly scheduled full vendor payments to

the factor. As of February 3, 2007 and January 28, 2006, the Company had an outstanding balance of

$13,990 and $11,156, respectively, under these arrangements, classified as trade payable program liability

in the consolidated balance sheets.

The other notes payable have a principal balance of $268 and $1,315 and a weighted average interest

rate of 8.0% and 5.1% at February 3, 2007 and January 28, 2006, respectively, and mature at various times

through August 2016. Certain of these notes are collateralized by land and buildings with an aggregate

carrying value of approximately $1,774 and $6,744 at February 3, 2007 and January 28, 2006, respectively.

CONVERTIBLE DEBT

February 3,

2007

January 28,

2006

4.25% Senior convertible notes, due June 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $— $119,000

Lesscurrentmaturities.................................................. — —

Total Long-Term Convertible Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $— $119,000

On October 27, 2006, the Company amended and restated its Senior Secured Term Loan Facility to

increase its size from $200,000 to $320,000. Proceeds from the facility were used to satisfy and discharge

the Company’s outstanding $119,000 4.25% Convertible Senior Notes due June 1, 2007 by deposit into an

escrow fund with an independent trustee. The right of the holders of the convertible notes to convert them

into shares of the Company’s common stock, at any time until the June 1, 2007 maturity date, survives such

satisfaction and discharge. The conversion price is approximately $22.40 per share. The Company recorded

non-cash charges for the value of such conversion right, approximately $755 as determined by the Black-

Scholes method, and $430 for deferred financing cost.

OTHER

Several of the Company’s debt agreements require the maintenance of certain financial ratios and

compliance with covenants. The most restrictive of these covenants, an EBITDA requirement, is triggered

if the Company’s availability under its line of credit agreement drops below $50,000. As of February 3,

2007 the Company had an availability of approximately $190,000 under its line of credit, and was in

compliance with all covenants contained in its debt agreements.