Pep Boys 2006 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2006 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

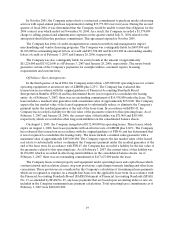

26

The Company believes that the following represent its more critical estimates and assumptions used in

the preparation of the consolidated financial statements, although not inclusive:

•The Company evaluates whether inventory is stated at the lower of cost or market based on

historical experience with the carrying value and life of inventory. The assumptions used in this

evaluation are based on current market conditions and the Company believes inventory is stated at

the lower of cost or market in the consolidated financial statements. In addition, historically the

Company has been able to return excess items to vendors for credit. Future changes in vendors, in

their policies or in their willingness to accept returns of excess inventory could require a revision in

the estimates. If our estimates regarding excess or obsolete inventory are inaccurate, we may be

exposed to losses or gains that could be material. A 10% difference in these estimates at February 3,

2007 would have affected net earnings by approximately $428,000 for the fiscal year ended

February 3, 2007.

•The Company has risk participation arrangements with respect to casualty and health care

insurance, including the maintaining of stop loss coverage with third party insurers to limit our total

exposure. A reserve for the liabilities associated with these agreements is established using actuarial

methods followed in the insurance industry and our historical claims experience. The amounts

included in the Company’s costs related to these arrangements are estimated and can vary based on

changes in assumptions, claims experience or the providers included in the associated insurance

programs. A 10% change in our self-insurance liabilities at February 3, 2007 would have affected

net earnings by approximately $2,723,000 for the fiscal year ended February 3, 2007.

•The Company records reserves for future product returns, warranty claims and inventory shrinkage.

The reserves are based on current sales of products and historical claims and inventory shrinkage

experience. If actual experience differs from historical levels, revisions in the Company’s estimates

may be required. A 10% change in these reserves at February 3, 2007 would have affected net

earnings by approximately $329,000 for the fiscal year ended February 3, 2007.

•The Company has significant pension costs and liabilities that are developed from actuarial

valuations. Inherent in these valuations are key assumptions including discount rates, expected

return on plan assets, mortality rates and merit and promotion increases. The Company is required

to consider current market conditions, including changes in interest rates, in selecting these

assumptions. Changes in the related pension costs or liabilities may occur in the future due to

changes in the assumptions. The following table highlights the sensitivity of our pension obligations

and expense to changes in these assumptions, assuming all other assumptions remain constant:

Change in Assumption

Impact on Annual

Pension Expense

Impact on Projected

Benefit Obligation

0.50 percentage point decrease in discount rate . . . . . . . . . . . . Increase $480,000 Increase $3,795,000

0.50 percentage point increase in discount rate . . . . . . . . . . . . Decrease $480,000 Decrease $3,795,000

5.0% decrease in expected rate of return on assets . . . . . . . . . Increase $187,000 —

5.0% increase in expected rate of return on assets. . . . . . . . . . Decrease $187,000 —

•The Company periodically evaluates its long-lived assets for indicators of impairment.

Management’s judgments are based on market and operational conditions at the time of evaluation.

Future events could cause management’s conclusion on impairment to change, requiring an

adjustment of these assets to their then current fair market value.

•We have a share-based compensation plan, which includes stock options and restricted stock units,

or RSUs. We account for our share-based compensation plans as prescribed by the fair value

provisions of SFAS No. 123R. We determine the fair value of our stock options at the date of the

grant using the Black-Scholes option-pricing model. The RSUs are awarded at a price equal to the