Pep Boys 2006 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2006 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

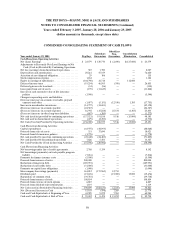

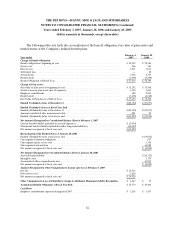

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 3, 2007, January 28, 2006 and January 29, 2005

(dollar amounts in thousands, except share data)

68

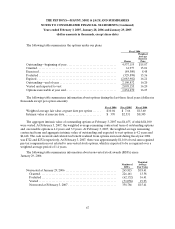

The following table summarizes information about RSUs during the last three fiscal years (dollars in

thousands except per unit amount):

Fiscal 2006 Fiscal 2005 Fiscal 2004

Weighted average fair value at grant date per unit . . . . . . . . $13.58 $16.71 $22.41

Fair Value at vesting date. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,660 $ 881 $ 8

Intrinsic value at conversion date . . . . . . . . . . . . . . . . . . . . . . . $1,075 $ 679 $ 5

Tax benefits realized from conversions . . . . . . . . . . . . . . . . . . $ 734 $ 248 $ 3

At February 3, 2007, there was approximately $3,370 of total unrecognized pre-tax compensation cost

related to non-vested RSUs, which is expected to be recognized over a weighted-average period of

1.7 years.

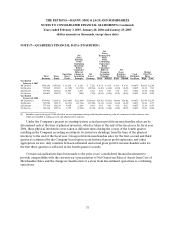

NOTE 12—ASSET RETIREMENT OBLIGATIONS

At February 3, 2007, the Company has a liability pertaining to the asset retirement obligation in

accrued expenses and other long-term liabilities on its consolidated balance sheet. The following is a

reconciliation of the beginning balance and ending carrying amounts of the Company’s asset retirement

obligation under SFAS 143 from January 29, 2005 through February 3, 2007:

Assetretirementobligation,January29,2005........................... $ 5,057

Assetretirementobligationincurredduringtheperiod................. 43

Assetretirementobligationsettledduringtheperiod .................. (141)

Accretionexpense................................................. 109

Reductioninassetretirementliability................................ (1,945)

AdoptionofFIN47................................................ 3,652

Assetretirementobligation,January28,2006........................... 6,775

Assetretirementobligationincurredduringtheperiod................. 131

Asset retirement obligation settled during the period . . . . . . . . . . . . . . . . . . (130)

Accretionexpense................................................. 269

Assetretirementobligation,February3,2007........................... $ 7,045

In the fourth quarter of fiscal 2005, the Company reviewed and revised its estimated settlement costs.

The Company reversed $1,945 of the liability as the original estimates of the contamination occurrence

rate and the cost to remediate such contaminations proved to be higher than actual experience is yielding.

The Company adopted FIN 47, “Accounting for Conditional Asset Retirement Obligations,” an

interpretation of SFAS 143, “Asset Retirement Obligations” on January 28, 2006. This interpretation

impacted the Company in recognition of legal obligations associated with surrendering its leased

properties. These obligations were previously omitted from the Company’s SFAS 143 analysis due to their

uncertain timing. The impact of adopting FIN 47 was the recognition of net additional leasehold

improvement assets amounting to $470, an asset retirement obligation of $3,652 and a charge of $3,182

($2,021, net of tax), which was included in Cumulative Effect of Change in Accounting Principle in the

accompanying consolidated statement of operations for fiscal year 2005.