Lenovo 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 Lenovo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

2008/09 Annual Report Lenovo Group Limited

95

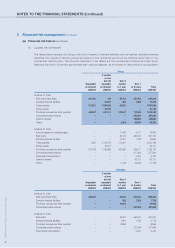

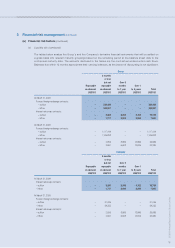

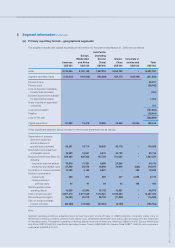

3 Financial risk management (continued)

(a) Financial risk factors (continued)

(iv) Credit risk

Credit risk is managed on a group basis. Credit risk arises from cash and cash equivalents, derivative financial

instruments and deposits with banks and financial institutions, as well as credit exposures to customers, including

outstanding receivables and committed transactions.

For banks and other financial institutions, the Group controls its credit risk through monitoring their credit rating and

setting approved counterparty credit limits that are regularly reviewed.

The Group has no significant concentration of customer credit risk. The Group has a credit policy in place and

exposures to these credit risks are monitored on an ongoing basis.

No credit limits were exceeded during the reporting period, and management does not expect any losses from non-

performance by these counterparties.

(v) Liquidity risk

Prudent liquidity risk management includes maintaining sufficient cash and marketable securities, the availability of

funding from an adequate amount of committed credit facilities and the ability to close out market positions. Due

to the dynamic nature of the underlying businesses, Group Treasury maintains flexibility by maintaining availability

of funding under committed credit lines.

Management monitors rolling forecasts of the Group’s liquidity reserve comprises undrawn borrowing facility (Note

33), bank deposits and cash and cash equivalents (Note 26) on the basis of expected cash flows.