Lenovo 2009 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2009 Lenovo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

2008/09 Annual Report Lenovo Group Limited

87

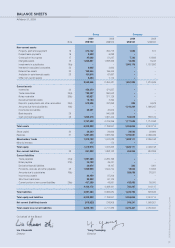

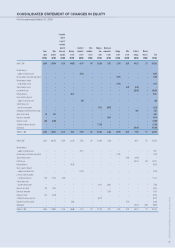

2 Significant accounting policies (continued)

(h) Financial assets (continued)

Changes in the fair value of monetary securities denominated in a foreign currency and classified as available-for-sale are

analyzed between translation differences resulting from changes in amortized cost of the security and other changes in

the carrying amount of the security. The translation differences on monetary securities are recognized in profit or loss,

while translation differences on non-monetary securities are recognized in equity. Changes in the fair value of monetary

and non-monetary securities classified as available-for-sale are recognized in equity.

When securities classified as available-for-sale are sold or impaired, the accumulated fair value adjustments recognized

in equity are included in the income statement as gains or losses from investment securities.

Interest on available-for-sale securities calculated using the effective interest method is recognized in the income

statement as part of other income. Dividends on available-for-sale equity instruments are recognized in the income

statement as part of other income when the Group’s right to receive payments is established.

The fair values of quoted investments are based on current bid prices. If the market for a financial asset is not active (and

for unlisted securities), the Group establishes fair value by using valuation techniques. These include the use of recent

arm’s length transactions, reference to other instruments that are substantially the same, discounted cash flow analysis,

and option pricing models refined to reflect the issuer’s specific circumstances.

The Group assesses at each balance sheet date whether there is objective evidence that a financial asset or a group

of financial assets is impaired. In the case of equity securities classified as available-for-sale, a significant or prolonged

decline in the fair value of the security below its cost is considered in determining whether the securities are impaired. If

any such evidence exists for available-for-sale financial assets, the cumulative loss, measured as the difference between

the acquisition cost and the current fair value, less any impairment loss on that financial asset previously recognized in

the income statement, is removed from equity and recognized in the income statement. Impairment losses recognized in

the income statement on equity instruments are not reversed through the income statement. Impairment testing of trade

receivables is described in Note 2(k).

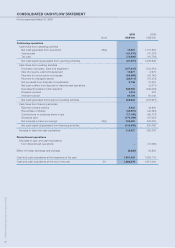

(i) Derivative financial instruments and hedging activities

Derivatives are initially recognized at fair value on the date a derivative contract is entered into and are subsequently

remeasured at their fair value. The method of recognizing the resulting gain or loss depends on whether the derivative

is designated as a hedging instrument, and if so, the nature of the item being hedged. The Group designates certain

derivatives as either: (1) hedges of the fair value of recognized assets or liabilities or a firm commitment (fair value hedge)

or (2) hedges of highly probable forecast transactions (cash flow hedges).

The Group documents at the inception of the transaction the relationship between hedging instruments and hedged

items, as well as its risk management objectives and strategy for undertaking various hedge transactions. The Group

also documents its assessment, both at hedge inception and on an ongoing basis, of whether the derivatives that are

used in hedging transactions are highly effective in offsetting changes in fair values or cash flows of hedged items.

(i) Fair value hedge

Changes in the fair value of derivatives that are designated and qualified as fair value hedges are recorded in the

income statement, together with any changes in the fair value of the hedged asset or liability that are attributable to

the hedged risk.