Chrysler 2008 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2008 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

|

|

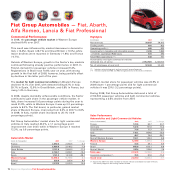

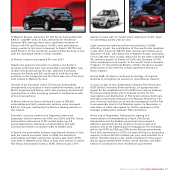

Report on Operations Fiat Group Automobiles 71

In Western Europe, deliveries for Fiat Group Automobiles fell

8.8% to 1,237,900 units. In Italy, deliveries for the Sector

declined 16%, whereas there were significant increases in

France (+30.7%) and Germany (+14.4%), with performance

being counter to the trend in demand. In Spain (-38.7%) and

Great Britain (-8.1%), the Sector posted marked declines in line

with the downward trends in those markets.

In Poland, volumes increased 6.5% over 2007.

Despite the general contraction in volumes, the Sector’s

products performed well: the Lancia Delta and Alfa MiTo, new

models introduced during the year, achieved increasing

success; the Panda and 500 continued to hold the top two

positions in the A segment and the Punto was one of the most

sold models in Western Europe.

Outside of the European Union, Fiat Group Automobiles

strengthened its presence in well-established markets, such as

Brazil, Argentina and Turkey, while also pursuing development

opportunities in other emerging markets in collaboration with

strong local partners.

In Brazil, where the Sector delivered a total of 665,600

automobiles and light commercial vehicles, sales increased

8.6% for the year, confirming the Sector’s leading position in

this market.

Economic recovery continued in Argentina, where the

passenger vehicle market rose 6.6% over 2007, and Fiat Group

Automobiles achieved an 11.9% market share (up 0.8

percentage points). Deliveries of automobiles and light

commercial vehicles increased 15.9% to 65,600 units.

In Turkey, the automobile industry experienced declines in line

with the overall economic trend. In 2008, the market for

automobiles and light commercial vehicles was down 16.9%

over 2007 to 494,000 units. Tofas (a local joint venture in which

Fiat Group Automobiles holds a 37.9% interest) saw a 21%

decline in sales with its market share slipping to 12.4%, down

0.7 percentage points year on year.

Light commercial vehicles performed positively in 2008,

reflecting, in part, the contribution of the new Fiorino launched

in late 2007. A total of 408,700 light commercial vehicles were

delivered (+5.3%), with deliveries in Western Europe increasing

1.1% to 241,000 units. In Italy, deliveries for the Sector declined

3%, whereas growth in France (+31.2%) and Germany (+7.1%)

either surpassed or ran counter to the overall trend in demand.

In Spain (-31.1%) and Great Britain (-18.3%), the Sector posted

performance in line with the overall significant declines in

those markets.

During 2008, the Sector continued its strategy of targeted

alliances to strengthen its position in international markets.

In June, as part of the collaboration between Fiat Group and

OJSC-Sollers (formerly Severstal-Auto), an agreement was

signed for the establishment of a 50/50 joint venture between

Fiat Group Automobiles and its Russian partner for the

manufacture and distribution of Fiat brand vehicles (both cars

and light commercial vehicles) in the Russian Federation. The

joint venture’s activities are to include management of the Fiat

Linea assembly plant in the Tatarstan region. In November, a

new letter of intent was signed for further expansion of the

strategic collaboration between FGA and Sollers.

At the end of September, following the signing of a

memorandum of understanding in April, Fiat Group

Automobiles and the Serbian government announced a

definitive agreement for the creation of a joint venture to

produce cars at the Zastava plant in Kragujevac. The company

will be held 67% by FGA and 33% by the Serbian government.

Once fully operational (in 2010), the plant will have a production

capacity of some 200,000 vehicles per year, with potential for a

further 100,000 units per year. Initial investment in the project

will be approximately €700 million, which includes over €200

million in contributions from the Serbian government.