Chrysler 2008 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2008 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

|

|

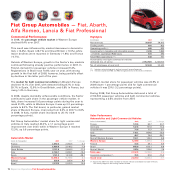

Report on Operations Fiat Group Automobiles70

Fiat Group Automobiles — Fiat, Abarth,

Alfa Romeo, Lancia & Fiat Professional

Commercial Performance

In 2008, the passenger vehicle market in Western Europe

declined 8.4% over 2007.

This result was influenced by marked decreases in demand in

Italy (-13.4%), Spain (-28.1%) and Great Britain (-11.3%), while

lesser declines were reported in Germany (-1.8%) and France

(-0.7%).

Outside of Western Europe, growth in the Sector’s key markets

continued following already positive performance in 2007. In

Poland, demand for passenger vehicles increased 9.4%.

Registrations in Brazil rose 10.6% year on year, with strong

growth in the first half of 2008, however, being partially offset

by declines in the latter part of the year.

The market for light commercial vehicles in Western Europe

declined 10.1% over 2007, with demand falling 8.7% in Italy,

39.7% in Spain, 12.9% in Great Britain, and 0.8% in France, but

rising 1.4% in Germany.

In 2008, despite decidedly unfavourable conditions, the Sector

continued to gain share in the passenger vehicle market. In

Italy, share increased 0.6 percentage points during the year to

reach 31.9%, while in Western Europe it was up 0.2 percentage

points to 8.2%. The Fiat brand, in particular, gained market

share in Western Europe, improving from 6.2% in 2007 to 6.6%

in 2008. In Italy, market share increased to 25.1% (+0.9

percentage points).

Fiat Group Automobiles’ market share for light commercial

vehicles in Italy reached 43.2%, a 1.1 percentage point

improvement over 2007, while in Western Europe it reached

12.3%, up 0.6 percentage points.

In Brazil, market share for passenger vehicles was 24.9% in

2008 (down 1 percentage point) and for light commercial

vehicles it was 23% (-3.2 percentage points).

During 2008, Fiat Group Automobiles delivered a total of

2,152,500 passenger vehicles and light commercial vehicles,

representing a 3.6% decline from 2007.

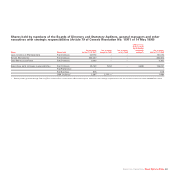

Highlights

(€ millions) 2008 2007

Net revenues 26,937 26,812

Trading profit 691 803

Operating profit (*) 460 635

Investments in tangible and intangible assets 2,288 1,865

- of which, capitalised R&D costs 641 493

Total R&D expenditure (**) 843 751

Automobiles and light commercial vehicles

delivered (no. of units) 2,152,500 2,233,800

No. of employees at year end 52,634 50,542

(*) Includes restructuring costs and net unusual income/(expense).

(**) Includes capitalised R&D and R&D charged directly to the income statement.

Automobile Market

(units in thousands) 2008 2007 % change

France 2,050.3 2,064.5 -0.7

Germany 3,090.0 3,148.2 -1.8

Great Britain 2,131.8 2,404.0 -11.3

Italy 2,160.1 2,493.1 -13.4

Spain 1,161.2 1,614.8 -28.1

Western Europe 13,558.4 14,797.6 -8.4

Poland 320.0 292.4 9.4

Brazil 2,237.3 2,022.3 10.6

Sales Performance

Automobiles and Light Commercial Vehicles

(units in thousands) 2008 2007 % change

France 123.8 94.7 30.7

Germany 122.8 107.3 14.4

Great Britain 71.4 77.7 -8.1

Italy 718.1 854.6 -16.0

Spain 48.7 79.4 -38.7

Rest of Western Europe 153.1 143.3 6.8

Western Europe 1,237.9 1,357.0 -8.8

Poland 41,6 39.1 6.5

Brazil 665.6 613.1 8.6

Rest-of-World 207.4 224.6 -7.6

Total sales 2,152.5 2,233.8 -3.6

Associate companies (*) 76.5 90.6 -15.5

Grand total 2,229.0 2,324.4 -4.1

(*) Figures for 2007 have been restated to include vehicles assembled and sold in Russia.

This activity began in the closing months of 2007.