Cablevision 2014 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2014 Cablevision annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

34

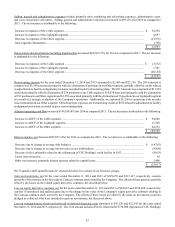

The Company assesses these qualitative factors to determine whether it is necessary to perform the two-step quantitative goodwill

impairment test. This quantitative test is required only if the Company concludes that it is more likely than not that a reporting

unit's fair value is less than its carrying amount.

When the qualitative assessment is not used, or if the qualitative assessment is not conclusive, the Company is required to determine

goodwill impairment using a two-step process. The first step of the goodwill impairment test is used to identify potential impairment

by comparing the fair value of a reporting unit with its carrying amount, including goodwill utilizing an enterprise-value based

premise approach. If the carrying amount of a reporting unit exceeds its fair value, the second step of the goodwill impairment

test is performed to measure the amount of impairment loss, if any. The second step of the goodwill impairment test compares

the implied fair value of the reporting unit's goodwill with the carrying amount of that goodwill. If the carrying amount of the

reporting unit's goodwill exceeds the implied fair value of that goodwill, an impairment loss is recognized in an amount equal to

that excess. The implied fair value of goodwill is determined in the same manner as the amount of goodwill that would be recognized

in a business combination. For the purpose of evaluating goodwill impairment at the annual impairment test date, the Company

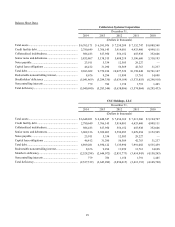

had two reporting units containing approximately 97% of the Company's goodwill balance of $264,690. These reporting units are

Cable ($234,290) and Lightpath ($21,487).

The Company assesses the qualitative factors discussed above to determine whether it is necessary to perform the one-step

quantitative identifiable indefinite-lived intangible assets impairment test. This quantitative test is required only if the Company

concludes that it is more likely than not that a unit of accounting’s fair value is less than its carrying amount. When the qualitative

assessment is not used, or if the qualitative assessment is not conclusive, the impairment test for identifiable indefinite-lived

intangible assets requires a comparison of the estimated fair value of the intangible asset with its carrying value. If the carrying

value of the intangible asset exceeds its fair value, an impairment loss is recognized in an amount equal to that excess. The

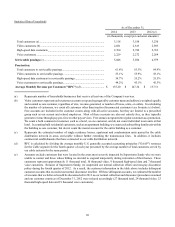

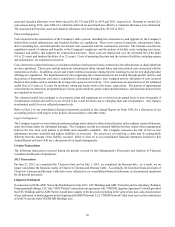

following table sets forth the amount of identifiable indefinite-lived intangible assets reported in the Company's consolidated

balance sheet as of December 31, 2014:

Reportable Segment Unit of Accounting

Identifiable

Indefinite-

Lived Intangible

Assets Balance

Cable ................................................................... Cable Television Franchises................................... $ 731,848

Other.................................................................... Newsday Trademarks.............................................. 7,000

Cable ................................................................... Other indefinite-lived intangibles........................... 250

$ 739,098

For other long-lived assets, including intangible assets that are amortized, the Company evaluates assets for recoverability when

there is an indication of potential impairment. If the undiscounted cash flows from a group of assets being evaluated is less than

the carrying value of that group of assets, the fair value of the asset group is determined and the carrying value of the asset group

is written down to fair value.

In assessing the recoverability of the Company's goodwill and other long-lived assets, the Company must make assumptions

regarding estimated future cash flows and other factors to determine the fair value of the respective assets. These estimates and

assumptions could have a significant impact on whether an impairment charge is recognized and also the magnitude of any such

charge. Fair value estimates are made at a specific point in time, based on relevant information. These estimates are subjective

in nature and involve uncertainties and matters of significant judgments and therefore cannot be determined with precision. Changes

in assumptions could significantly affect the estimates. Estimates of fair value are primarily determined using discounted cash

flows and comparable market transactions. These valuations are based on estimates and assumptions including projected future

cash flows, discount rate, determination of appropriate market comparables and determination of whether a premium or discount

should be applied to comparables. For the Cable reportable segment, these valuations also include assumptions for average annual

revenue per customer, number of serviceable passings, operating margin and market penetration as a percentage of serviceable

passings, among other assumptions. Further, the projected cash flow assumptions consider contractual relationships, customer

attrition, eventual development of new technologies and market competition. For Newsday, these valuations also include

assumptions for advertising and circulation revenue trends, operating margin, market participant synergies, and market multiples

for comparable companies. If these estimates or material related assumptions change in the future, the Company may be required

to record impairment charges related to its long-lived assets.