Burger King 2010 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2010 Burger King annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

Table of Contents

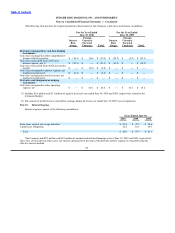

BURGER KING HOLDINGS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements — (Continued)

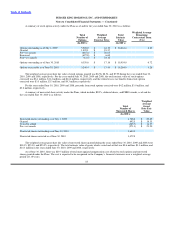

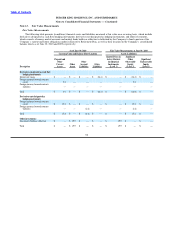

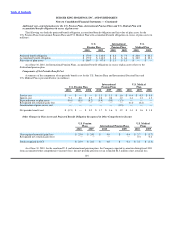

Interest Rate Swaps

The Company enters into receive−variable, pay−fixed interest rate swap contracts to hedge a portion of the Company’s forecasted

variable−rate interest payments on its underlying Term Loan A and Term Loan B−1 debt (the “Term Debt”). Interest payments on the

Term Debt are made quarterly and the variable rate on the Term Debt is reset at the end of each fiscal quarter. The interest rate swap

contracts are designated as cash flow hedges and to the extent they are effective in offsetting the variability of the variable−rate interest

payments, changes in the derivatives’ fair value are not included in current earnings but are included in accumulated other

comprehensive income (AOCI) in the accompanying consolidated balance sheets. These changes in fair value are subsequently

reclassified into earnings as a component of interest expense each quarter as interest payments are made on the Term Debt. At June 30,

2010, interest rate swap contracts with a notional amount of $575.0 million were outstanding.

In September 2006, the Company settled interest rate swaps designated as cash flow hedges, which had a fair value of

$11.5 million, and terminated the hedge relationship. The fair value of the settled swaps is recorded in AOCI and is being recognized as

a reduction to interest expense each quarter over the remaining term of the Term Debt. At June 30, 2010, $0.4 million remained in

AOCI related to settled interest rate swaps.

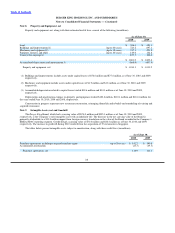

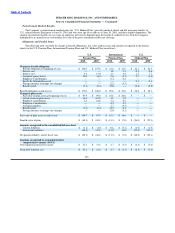

Foreign Currency Forward Contracts

The Company enters into foreign currency forward contracts, which typically have maturities between one and fifteen months, to

economically hedge the remeasurement of certain foreign currency−denominated intercompany loans receivable and other

foreign−currency denominated assets recorded in the Company’s consolidated balance sheets. Remeasurement represents changes in the

expected amount of cash flows to be received or paid upon settlement of the intercompany loan receivables and other foreign−currency

denominated assets and liabilities resulting from a change in currency exchange rates. The Company also enters into foreign currency

forward contracts in order to manage the foreign exchange variability in forecasted royalty cash flows due to fluctuations in exchange

rates. At June 30, 2010, foreign currency forward contracts with a notional amount of $391.2 million were outstanding.

Credit Risk

By entering into derivative instrument contracts, the Company exposes itself, from time to time, to counterparty credit risk.

Counterparty credit risk is the failure of the counterparty to perform under the terms of the derivative contract. When the fair value of a

derivative contract is in an asset position, the counterparty has a liability to the Company, which creates credit risk for the Company.

The Company attempts to minimize this risk by selecting counterparties with investment grade credit ratings, limiting its exposure to

any single counterparty and regularly monitoring its market position with each counterparty.

Credit−Risk Related Contingent Features

The Company’s derivative instruments do not contain any credit−risk related contingent features.

94