Berkshire Hathaway 2010 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2010 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

One not-so-small footnote: Under Tony, GEICO has developed one of the country’s largest personal-

lines insurance agencies, which primarily sells homeowners policies to our GEICO auto insurance customers. In

this business, we represent a number of insurers that are not affiliated with us. They take the risk; we simply sign

up the customers. Last year we sold 769,898 new policies at this agency operation, up 34% from the year before.

The obvious way this activity aids us is that it produces commission revenue; equally important is the fact that it

further strengthens our relationship with our policyholders, helping us retain them.

I owe an enormous debt to Tony and Davy (and, come to think of it, to that janitor as well).

************

Now, let’s examine the four major sectors of Berkshire. Each has vastly different balance sheet and

income characteristics from the others. Lumping them together therefore impedes analysis. So we’ll present them

as four separate businesses, which is how Charlie and I view them.

We will look first at insurance, Berkshire’s core operation and the engine that has propelled our

expansion over the years.

Insurance

Property-casualty (“P/C”) insurers receive premiums upfront and pay claims later. In extreme cases,

such as those arising from certain workers’ compensation accidents, payments can stretch over decades. This

collect-now, pay-later model leaves us holding large sums – money we call “float” – that will eventually go to

others. Meanwhile, we get to invest this float for Berkshire’s benefit. Though individual policies and claims

come and go, the amount of float we hold remains remarkably stable in relation to premium volume.

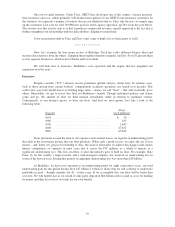

Consequently, as our business grows, so does our float. And how we have grown: Just take a look at the

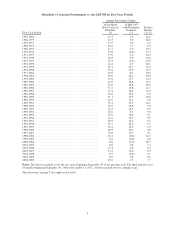

following table:

Yearend

Float

(in $ millions)

1970 ........................................ $ 39

1980 ........................................ 237

1990 ........................................ 1,632

2000 ........................................ 27,871

2010 ........................................ 65,832

If our premiums exceed the total of our expenses and eventual losses, we register an underwriting profit

that adds to the investment income that our float produces. When such a profit occurs, we enjoy the use of free

money – and, better yet, get paid for holding it. Alas, the wish of all insurers to achieve this happy result creates

intense competition, so vigorous in most years that it causes the P/C industry as a whole to operate at a

significant underwriting loss. This loss, in effect, is what the industry pays to hold its float. For example, State

Farm, by far the country’s largest insurer and a well-managed company, has incurred an underwriting loss in

seven of the last ten years. During that period, its aggregate underwriting loss was more than $20 billion.

At Berkshire, we have now operated at an underwriting profit for eight consecutive years, our total

underwriting gain for the period having been $17 billion. I believe it likely that we will continue to underwrite

profitably in most – though certainly not all – future years. If we accomplish that, our float will be better than

cost-free. We will benefit just as we would if some party deposited $66 billion with us, paid us a fee for holding

its money and then let us invest its funds for our own benefit.

10