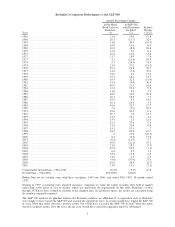

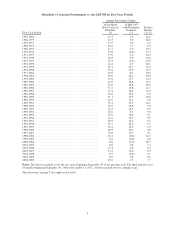

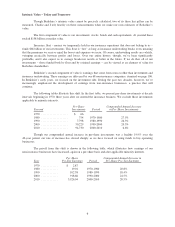

Berkshire Hathaway 2010 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2010 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

When I took control of Berkshire in 1965, I didn’t exploit this advantage. Berkshire was then only in

textiles, where it had in the previous decade lost significant money. The dumbest thing I could have done was to

pursue “opportunities” to improve and expand the existing textile operation – so for years that’s exactly what I

did. And then, in a final burst of brilliance, I went out and bought another textile company. Aaaaaaargh!

Eventually I came to my senses, heading first into insurance and then into other industries.

There is even a supplement to this world-is-our-oyster advantage: In addition to evaluating the

attractions of one business against a host of others, we also measure businesses against opportunities available in

marketable securities, a comparison most managements don’t make. Often, businesses are priced ridiculously

high against what can likely be earned from investments in stocks or bonds. At such moments, we buy securities

and bide our time.

Our flexibility in respect to capital allocation has accounted for much of our progress to date. We have

been able to take money we earn from, say, See’s Candies or Business Wire (two of our best-run businesses, but

also two offering limited reinvestment opportunities) and use it as part of the stake we needed to buy BNSF.

Our final advantage is the hard-to-duplicate culture that permeates Berkshire. And in businesses,

culture counts.

To start with, the directors who represent you think and act like owners. They receive token

compensation: no options, no restricted stock and, for that matter, virtually no cash. We do not provide them

directors and officers liability insurance, a given at almost every other large public company. If they mess up

with your money, they will lose their money as well. Leaving my holdings aside, directors and their families own

Berkshire shares worth more than $3 billion. Our directors, therefore, monitor Berkshire’s actions and results

with keen interest and an owner’s eye. You and I are lucky to have them as stewards.

This same owner-orientation prevails among our managers. In many cases, these are people who have

sought out Berkshire as an acquirer for a business that they and their families have long owned. They came to us

with an owner’s mindset, and we provide an environment that encourages them to retain it. Having managers

who love their businesses is no small advantage.

Cultures self-propagate. Winston Churchill once said, “You shape your houses and then they shape

you.” That wisdom applies to businesses as well. Bureaucratic procedures beget more bureaucracy, and imperial

corporate palaces induce imperious behavior. (As one wag put it, “You know you’re no longer CEO when you

get in the back seat of your car and it doesn’t move.”) At Berkshire’s “World Headquarters” our annual rent is

$270,212. Moreover, the home-office investment in furniture, art, Coke dispenser, lunch room, high-tech

equipment – you name it – totals $301,363. As long as Charlie and I treat your money as if it were our own,

Berkshire’s managers are likely to be careful with it as well.

Our compensation programs, our annual meeting and even our annual reports are all designed with an

eye to reinforcing the Berkshire culture, and making it one that will repel and expel managers of a different bent.

This culture grows stronger every year, and it will remain intact long after Charlie and I have left the scene.

We will need all of the strengths I’ve just described to do reasonably well. Our managers will deliver;

you can count on that. But whether Charlie and I can hold up our end in capital allocation depends in part on the

competitive environment for acquisitions. You will get our best efforts.

GEICO

Now let me tell you a story that will help you understand how the intrinsic value of a business can far

exceed its book value. Relating this tale also gives me a chance to relive some great memories.

Sixty years ago last month, GEICO entered my life, destined to shape it in a huge way. I was then a

20-year-old graduate student at Columbia, having elected to go there because my hero, Ben Graham, taught a

once-a-week class at the school.

8