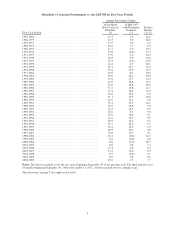

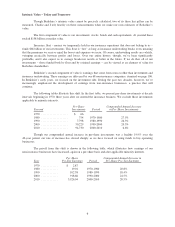

Berkshire Hathaway 2010 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2010 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

One day at the library, I checked out Ben’s entry in Who’s Who in America and found he was

chairman of Government Employees Insurance Co. (now called GEICO). I knew nothing of insurance and had

never heard of the company. The librarian, however, steered me to a large compendium of insurers and, after

reading the page on GEICO, I decided to visit the company. The following Saturday, I boarded an early train for

Washington.

Alas, when I arrived at the company’s headquarters, the building was closed. I then rather frantically

started pounding on a door, until finally a janitor appeared. I asked him if there was anyone in the office I could

talk to, and he steered me to the only person around, Lorimer Davidson.

That was my lucky moment. During the next four hours, “Davy” gave me an education about both

insurance and GEICO. It was the beginning of a wonderful friendship. Soon thereafter, I graduated from

Columbia and became a stock salesman in Omaha. GEICO, of course, was my prime recommendation, which got

me off to a great start with dozens of customers. GEICO also jump-started my net worth because, soon after

meeting Davy, I made the stock 75% of my $9,800 investment portfolio. (Even so, I felt over-diversified.)

Subsequently, Davy became CEO of GEICO, taking the company to undreamed-of heights before it got

into trouble in the mid-1970s, a few years after his retirement. When that happened – with the stock falling by

more than 95% – Berkshire bought about one-third of the company in the market, a position that over the years

increased to 50% because of GEICO’s repurchases of its own shares. Berkshire’s cost for this half of the business

was $46 million. (Despite the size of our position, we exercised no control over operations.)

We then purchased the remaining 50% of GEICO at the beginning of 1996, which spurred Davy, at 95,

to make a video tape saying how happy he was that his beloved GEICO would permanently reside with

Berkshire. (He also playfully concluded with, “Next time, Warren, please make an appointment.”)

A lot has happened at GEICO during the last 60 years, but its core goal – saving Americans substantial

money on their purchase of auto insurance – remains unchanged. (Try us at 1-800-847-7536 or

www.GEICO.com.) In other words, get the policyholder’s business by deserving his business. Focusing on this

objective, the company has grown to be America’s third-largest auto insurer, with a market share of 8.8%.

When Tony Nicely, GEICO’s CEO, took over in 1993, that share was 2.0%, a level at which it had

been stuck for more than a decade. GEICO became a different company under Tony, finding a path to consistent

growth while simultaneously maintaining underwriting discipline and keeping its costs low.

Let me quantify Tony’s achievement. When, in 1996, we bought the 50% of GEICO we didn’t already

own, it cost us about $2.3 billion. That price implied a value of $4.6 billion for 100%. GEICO then had tangible

net worth of $1.9 billion.

The excess over tangible net worth of the implied value – $2.7 billion – was what we estimated

GEICO’s “goodwill” to be worth at that time. That goodwill represented the economic value of the policyholders

who were then doing business with GEICO. In 1995, those customers had paid the company $2.8 billion in

premiums. Consequently, we were valuing GEICO’s customers at about 97% (2.7/2.8) of what they were

annually paying the company. By industry standards, that was a very high price. But GEICO was no ordinary

insurer: Because of the company’s low costs, its policyholders were consistently profitable and unusually loyal.

Today, premium volume is $14.3 billion and growing. Yet we carry the goodwill of GEICO on our

books at only $1.4 billion, an amount that will remain unchanged no matter how much the value of GEICO

increases. (Under accounting rules, you write down the carrying value of goodwill if its economic value

decreases, but leave it unchanged if economic value increases.) Using the 97%-of-premium-volume yardstick we

applied to our 1996 purchase, the real value today of GEICO’s economic goodwill is about $14 billion. And this

value is likely to be much higher ten and twenty years from now. GEICO – off to a strong start in 2011 – is the

gift that keeps giving.

9