Berkshire Hathaway 2008 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2008 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

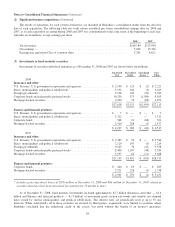

Notes to Consolidated Financial Statements (Continued)

(1) Significant accounting policies and practices (Continued)

(r) Accounting pronouncements adopted in 2008 and 2007 (Continued)

159, an entity may elect the fair value option for eligible items that existed at the adoption date. Berkshire did not

elect the fair value option for any eligible items.

In September 2008, the FASB issued FSP FAS 133-1 and FIN 45-4 “Disclosures about Derivatives and Certain

Guarantees” (“FSP FAS 133-1”), which requires sellers of credit derivatives to disclose additional information about

credit derivatives and is effective for periods ending after November 15, 2008. The adoption of FSP FAS 133-1 had

no material impact on Berkshire’s Consolidated Financial Statements.

Effective January 1, 2007, Berkshire adopted FASB Interpretation No. 48 “Accounting for Uncertainty in Income

Taxes-an interpretation of FASB Statement No. 109” (“FIN 48”). Under FIN 48, a tax position taken is recognized if

it is determined that the position will “more-likely-than-not” be sustained upon examination by a taxing authority. FIN

48 also establishes measurement guidance with respect to positions that have met the recognition threshold. The

cumulative effect of adoption of FIN 48 was a decrease of $24 million in retained earnings.

Effective January 1, 2007, Berkshire adopted FASB Staff Position No. AUG AIR-1 “Accounting for Planned Major

Maintenance Activities” (“AUG AIR-1”). AUG AIR-1 prohibits the accrual of liabilities in periods before the maintenance

is performed. Berkshire elected to use the direct expense method where maintenance costs are expensed as incurred.

Previously, certain maintenance costs related to the fractional aircraft ownership business were accrued in advance. The

cumulative effect of this accounting change of $52 million was recorded as an increase in retained earnings.

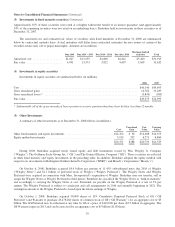

(s) Accounting pronouncements to be adopted in the future

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (“SFAS 141R”). SFAS

141R changes the accounting model for business combinations from a cost allocation standard to a standard that

provides, with limited exceptions, for the recognition at fair value of all identifiable assets and liabilities (including

contingent assets and liabilities) of the business acquired, regardless of whether 100% or a lesser controlling interest

of the business is acquired. SFAS 141R defines the acquisition date of a business acquisition as the date on which

control is achieved (generally the closing date of the acquisition). SFAS 141R also provides that acquisition costs are

expensed when incurred and expands disclosures. SFAS 141R is effective for Berkshire with respect to business

acquisitions completed after December 31, 2008.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements

an amendment of ARB No. 51” (“SFAS 160”). SFAS 160 establishes accounting and reporting standards for

non-controlling interests in consolidated subsidiaries (formerly “minority interests”). SFAS 160 also amends certain

consolidation procedures for consistency with SFAS 141R. Under SFAS 160, non-controlling interests are reported in

the consolidated balance sheet as a separate component of shareholders’ equity. Changes in ownership interests where

the parent retains a controlling interest are to be reported as transactions affecting shareholders’ equity. Prior to the

effective date of SFAS 160, such transactions were reported as additional investment purchases (potentially resulting

in recognition of additional assets) or as sales (potentially resulting in realized gains or losses). SFAS 160 is effective

for Berkshire as of January 1, 2009. When adopted, SFAS 160 is applied prospectively except that the presentation

and disclosure requirements are applied retrospectively for all periods presented.

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities

— an amendment of FASB Statement No. 133” (“SFAS 161”). SFAS 161 requires enhanced disclosures about

(a) how and why derivative instruments are used, (b) how derivative instruments and related hedged items are

accounted for and (c) how derivative instruments and related hedged items affect an entity’s financial position,

financial performance and cash flows. SFAS 161 is effective for financial statements issued for fiscal years and

interim periods beginning after November 15, 2008.

In May 2008, the FASB issued SFAS No. 163, “Accounting for Financial Guarantee Insurance Contracts” (“SFAS

163”). SFAS 163 clarifies accounting standards applicable to financial guarantee insurance contracts and specifies

certain disclosures. SFAS 163 is effective for financial statements issued for fiscal years beginning after December 15,

2008, except certain disclosures were effective for periods beginning after June 30, 2008.

Berkshire is continuing to evaluate the impact that these new accounting standards will have on its consolidated

financial statements but currently does not anticipate that the adoption of these accounting pronouncements will have

a material effect on its consolidated financial position.

36