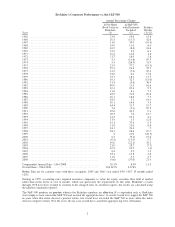

Berkshire Hathaway 2008 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2008 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

At that time, much of the industry employed sales practices that were atrocious. Writing about the

period somewhat later, I described it as involving “borrowers who shouldn’t have borrowed being financed by

lenders who shouldn’t have lent.”

To begin with, the need for meaningful down payments was frequently ignored. Sometimes fakery was

involved. (“That certainly looks like a $2,000 cat to me” says the salesman who will receive a $3,000

commission if the loan goes through.) Moreover, impossible-to-meet monthly payments were being agreed to by

borrowers who signed up because they had nothing to lose. The resulting mortgages were usually packaged

(“securitized”) and sold by Wall Street firms to unsuspecting investors. This chain of folly had to end badly, and

it did.

Clayton, it should be emphasized, followed far more sensible practices in its own lending throughout

that time. Indeed, no purchaser of the mortgages it originated and then securitized has ever lost a dime of

principal or interest. But Clayton was the exception; industry losses were staggering. And the hangover continues

to this day.

This 1997-2000 fiasco should have served as a canary-in-the-coal-mine warning for the far-larger

conventional housing market. But investors, government and rating agencies learned exactly nothing from the

manufactured-home debacle. Instead, in an eerie rerun of that disaster, the same mistakes were repeated with

conventional homes in the 2004-07 period: Lenders happily made loans that borrowers couldn’t repay out of their

incomes, and borrowers just as happily signed up to meet those payments. Both parties counted on “house-price

appreciation” to make this otherwise impossible arrangement work. It was Scarlett O’Hara all over again: “I’ll

think about it tomorrow.” The consequences of this behavior are now reverberating through every corner of our

economy.

Clayton’s 198,888 borrowers, however, have continued to pay normally throughout the housing crash,

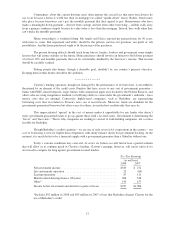

handing us no unexpected losses. This is not because these borrowers are unusually creditworthy, a point proved

by FICO scores (a standard measure of credit risk). Their median FICO score is 644, compared to a national

median of 723, and about 35% are below 620, the segment usually designated “sub-prime.” Many disastrous

pools of mortgages on conventional homes are populated by borrowers with far better credit, as measured by

FICO scores.

Yet at yearend, our delinquency rate on loans we have originated was 3.6%, up only modestly from

2.9% in 2006 and 2.9% in 2004. (In addition to our originated loans, we’ve also bought bulk portfolios of various

types from other financial institutions.) Clayton’s foreclosures during 2008 were 3.0% of originated loans

compared to 3.8% in 2006 and 5.3% in 2004.

Why are our borrowers – characteristically people with modest incomes and far-from-great credit

scores – performing so well? The answer is elementary, going right back to Lending 101. Our borrowers simply

looked at how full-bore mortgage payments would compare with their actual – not hoped-for – income and then

decided whether they could live with that commitment. Simply put, they took out a mortgage with the intention

of paying it off, whatever the course of home prices.

Just as important is what our borrowers did not do. They did not count on making their loan payments

by means of refinancing. They did not sign up for “teaser” rates that upon reset were outsized relative to their

income. And they did not assume that they could always sell their home at a profit if their mortgage payments

became onerous. Jimmy Stewart would have loved these folks.

Of course, a number of our borrowers will run into trouble. They generally have no more than minor

savings to tide them over if adversity hits. The major cause of delinquency or foreclosure is the loss of a job, but

death, divorce and medical expenses all cause problems. If unemployment rates rise – as they surely will in

2009 – more of Clayton’s borrowers will have troubles, and we will have larger, though still manageable, losses.

But our problems will not be driven to any extent by the trend of home prices.

11