Berkshire Hathaway 2008 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2008 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

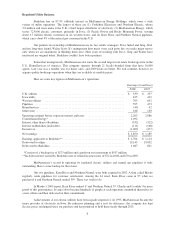

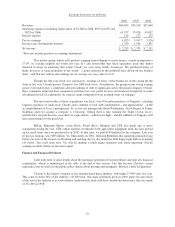

Unless facts or rules change, you will see these holdings reflected in our balance sheet at “equity

accounting” values, whatever their market prices. You will also see our share of their earnings (less applicable

taxes) regularly included in our quarterly and annual earnings.

I told you in an earlier part of this report that last year I made a major mistake of commission (and

maybe more; this one sticks out). Without urging from Charlie or anyone else, I bought a large amount of

ConocoPhillips stock when oil and gas prices were near their peak. I in no way anticipated the dramatic fall in

energy prices that occurred in the last half of the year. I still believe the odds are good that oil sells far higher in

the future than the current $40-$50 price. But so far I have been dead wrong. Even if prices should rise,

moreover, the terrible timing of my purchase has cost Berkshire several billion dollars.

I made some other already-recognizable errors as well. They were smaller, but unfortunately not that

small. During 2008, I spent $244 million for shares of two Irish banks that appeared cheap to me. At yearend we

wrote these holdings down to market: $27 million, for an 89% loss. Since then, the two stocks have declined

even further. The tennis crowd would call my mistakes “unforced errors.”

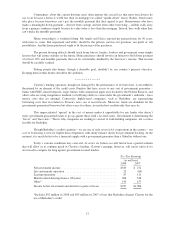

On the plus side last year, we made purchases totaling $14.5 billion in fixed-income securities issued

by Wrigley, Goldman Sachs and General Electric. We very much like these commitments, which carry high

current yields that, in themselves, make the investments more than satisfactory. But in each of these three

purchases, we also acquired a substantial equity participation as a bonus. To fund these large purchases, I had to

sell portions of some holdings that I would have preferred to keep (primarily Johnson & Johnson, Procter &

Gamble and ConocoPhillips). However, I have pledged – to you, the rating agencies and myself – to always run

Berkshire with more than ample cash. We never want to count on the kindness of strangers in order to meet

tomorrow’s obligations. When forced to choose, I will not trade even a night’s sleep for the chance of extra

profits.

The investment world has gone from underpricing risk to overpricing it. This change has not been

minor; the pendulum has covered an extraordinary arc. A few years ago, it would have seemed unthinkable that

yields like today’s could have been obtained on good-grade municipal or corporate bonds even while risk-free

governments offered near-zero returns on short-term bonds and no better than a pittance on long-terms. When the

financial history of this decade is written, it will surely speak of the Internet bubble of the late 1990s and the

housing bubble of the early 2000s. But the U.S. Treasury bond bubble of late 2008 may be regarded as almost

equally extraordinary.

Clinging to cash equivalents or long-term government bonds at present yields is almost certainly a

terrible policy if continued for long. Holders of these instruments, of course, have felt increasingly comfortable –

in fact, almost smug – in following this policy as financial turmoil has mounted. They regard their judgment

confirmed when they hear commentators proclaim “cash is king,” even though that wonderful cash is earning

close to nothing and will surely find its purchasing power eroded over time.

Approval, though, is not the goal of investing. In fact, approval is often counter-productive because it

sedates the brain and makes it less receptive to new facts or a re-examination of conclusions formed earlier.

Beware the investment activity that produces applause; the great moves are usually greeted by yawns.

Derivatives

Derivatives are dangerous. They have dramatically increased the leverage and risks in our financial

system. They have made it almost impossible for investors to understand and analyze our largest commercial

banks and investment banks. They allowed Fannie Mae and Freddie Mac to engage in massive misstatements of

earnings for years. So indecipherable were Freddie and Fannie that their federal regulator, OFHEO, whose more

than 100 employees had no job except the oversight of these two institutions, totally missed their cooking of the

books.

16