Anthem Blue Cross 2002 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2002 Anthem Blue Cross annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

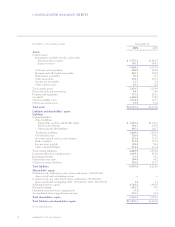

NOTES

to Consolidated Financial Statements (Continued)

Anthem, Inc. 2002 Annual Report 61

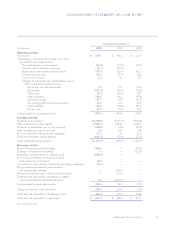

years for computer software. Leasehold improvements are

depreciated over the term of the related lease.

Goodwill and Other Intangible Assets: On January 1,

2002, the Company adopted FAS 141, Business Combina-

tions, and FAS 142, Goodwill and Other Intangible Assets.

FAS 141 requires business combinations completed after

June 30, 2001 to be accounted for using the purchase

method of accounting. It also specifies the types of

acquired intangible assets that are required to be recog-

nized and reported separately from goodwill. Under FAS

142, goodwill and other intangible assets with indefinite

lives are not amortized but are tested for impairment at

least annually. Goodwill represents the excess of cost of

acquisition over the fair value of net assets acquired.

Other intangible assets represent the values assigned to

subscriber bases, provider and hospital networks, Blue

Cross and Blue Shield trademarks, licenses, non-compete

and other agreements.

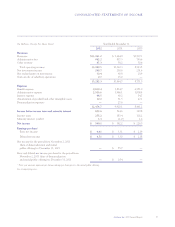

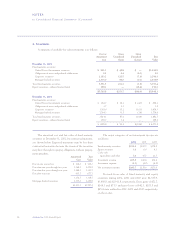

Policy Liabilities: Liabilities for unpaid claims include

estimated provisions for both reported and unreported

claims incurred on an undiscounted basis, as well as esti-

mated provisions for expenses related to the processing of

claims. The liabilities are adjusted regularly based on his-

torical experience and include estimates of trends in

claim severity and frequency and other factors, which

could vary as the claims are ultimately settled. Although

it is not possible to measure the degree of variability

inherent in such estimates, management believes these

liabilities are adequate.

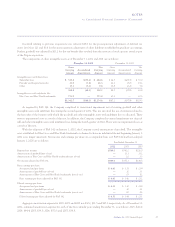

Future policy benefits include liabilities for life insur-

ance future policy benefits of $175.3 and $176.4 at

December 31, 2002 and 2001, respectively, and represent

primarily group term benefits determined using standard

industry mortality tables with interest rates ranging from

2.5% to 6.5%.

Other policyholder liabilities include certain case-

specific reserves as well as rate stabilization reserves asso-

ciated with retrospective rated insurance contracts. Rate

stabilization reserves represent accumulated premiums

that exceed what customers owe based on actual claim

experience and are paid based on contractual requirements.

Premium deficiency losses are recognized when it

is probable that expected claims and loss adjustment

expenses will exceed future premiums on existing health

and other insurance contracts without consideration of

investment income. For purposes of premium deficiency

losses, contracts are deemed to be either short or long

duration and are grouped in a manner consistent with the

Company’s method of acquiring, servicing and measuring

the profitability of such contracts. Once established, pre-

mium deficiency losses are amortized over the remaining

life of the contract.

Retirement Benefits: Retirement benefits represent out-

standing obligations for retiree medical, life, vision and

dental benefits and any unfunded liabilities related to

defined benefit pension plans. Unfunded liabilities for

pension benefits are accrued in accordance with FAS 87,

Employers’ Accounting for Pensions. Benefits for retiree

medical, life, vision and dental benefits are accrued in

accordance with FAS 106, Employers’ Accounting for

Postretirement Benefits Other Than Pensions.

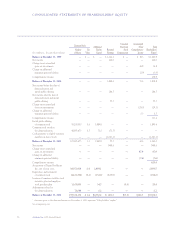

Comprehensive Income: Comprehensive income includes

net income, the change in unrealized gains (losses) on

investments and the change in the additional minimum

pension liability.

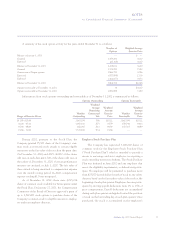

Revenue Recognition: Gross premiums for fully-insured

contracts are recognized as revenue over the period insur-

ance coverage is provided. Premiums applicable to the

unexpired contractual coverage periods are reflected in

the accompanying consolidated balance sheets as unearned

income. Premiums include revenue from retrospective

rated contracts where revenue is based on the estimated

ultimate loss experience of the contract. Premium rev-

enue includes an adjustment for retrospective rated

refunds based on an estimate of incurred claims. Premium

rates for certain lines of business are subject to approval

by the Department of Insurance of each respective state.

Administrative fees include revenue from certain

group contracts that provide for the group to be at risk for

all, or with supplemental insurance arrangements, a por-

tion of their claims experience. The Company charges

these self-funded groups an administrative fee, which is

based on the number of members in a group or the group’s

claim experience. In addition, administrative fees include

amounts received for the administration of Medicare or

certain other government programs. Such fees are based

on a percentage of the claim amounts processed or a com-

bination of a fixed fee per claim plus a percentage of the