The Hartford 2011 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

43

In specialty lines, many lines of insurance are “long-tail”, including large deductible workers’ compensation insurance, as such, reserve

estimates for these lines are more difficult to determine than reserve estimates for shorter-tail lines of insurance. Estimating required

reserve levels for large deductible workers’ compensation insurance is further complicated by the uncertainty of whether losses that are

attributable to the deductible amount will be paid by the insured; if such losses are not paid by the insured due to financial difficulties,

the Company would be contractually liable. Another example of reserve variability relates to reserves for directors’ and officers’

insurance. There is potential volatility in the required level of reserves due to the continued uncertainty regarding the number and

severity of class action suits, including uncertainty regarding the Company’ s exposure to losses arising from the collapse of the sub-

prime mortgage market. Additionally, the Company’ s exposure to losses under directors’ and officers’ insurance policies is primarily in

excess layers, making estimates of loss more complex. The recent financial market turmoil has increased the number of shareholder

class action lawsuits against our insureds or their directors and officers and this trend could continue for some period of time.

Impact of changes in key assumptions on reserve volatility

As stated above, the Company’ s practice is to estimate reserves using a variety of methods, assumptions and data elements. Within its

reserve estimation process for reserves other than asbestos and environmental, the Company does not consistently use statistical loss

distributions or confidence levels around its reserve estimate and, as a result, does not disclose reserve ranges.

The reserve estimation process includes assumptions about a number of factors in the internal and external environment. Across most

lines of business, the most important assumptions are future loss development factors applied to paid or reported losses to date. The

trend in loss costs is also a key assumption, particularly in the most recent accident years, where loss development factors are less

credible.

The following discussion includes disclosure of possible variation from current estimates of loss reserves due to a change in certain key

indicators of potential losses. Each of the impacts described below is estimated individually, without consideration for any correlation

among key indicators or among lines of business. Therefore, it would be inappropriate to take each of the amounts described below and

add them together in an attempt to estimate volatility for the Company’ s reserves in total. The estimated variation in reserves due to

changes in key indicators is a reasonable estimate of possible variation that may occur in the future, likely over a period of several

calendar years. It is important to note that the variation discussed is not meant to be a worst-case scenario, and therefore, it is possible

that future variation may be more than the amounts discussed below.

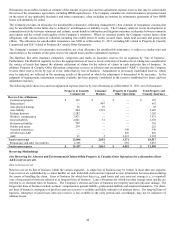

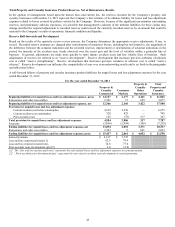

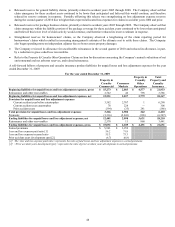

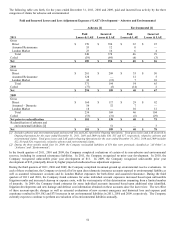

Recorded reserves for auto liability, net of reinsurance, are $2.1 billion across all lines, $1.5 billion of which is in Consumer Markets.

Personal auto liability reserves are shorter-tailed than other lines of business (such as workers’ compensation) and, therefore, less

volatile. However, the size of the reserve base means that future changes in estimates could be material to the Company’ s results of

operations in any given period. The key indicator for Consumer Markets auto liability is the annual loss cost trend, particularly the

severity trend component of loss costs. A 2.5 point change in annual severity for the two most recent accident years would change the

estimated net reserve need by $80, in either direction. A 2.5 point change in annual severity is within the Company’ s historical

variation.

Recorded reserves for workers’ compensation, net of reinsurance, are $7.5 billion. Loss development patterns are a key indicator for

this line of business, particularly for more mature accident years. Historically, loss development patterns have been impacted by, among

other things, medical cost inflation. The Company has reviewed the historical variation in reported loss development patterns. If the

reported loss development patterns change by 3%, the estimated net reserve need would change by $400, in either direction. A 3%

change in reported loss development patterns is within the Company’ s historical variation, as measured by the variation around the

average development factors as reported in statutory accident year reports.

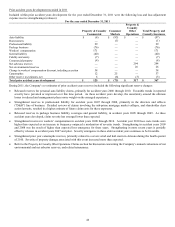

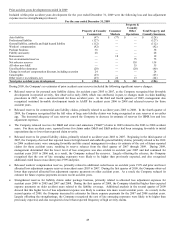

Recorded reserves for general liability, net of reinsurance, are $2.7 billion. Loss development patterns are a key indicator for this line of

business, particularly for more mature accident years. Historically, loss development patterns have been impacted by, among other

things, emergence of new types of claims (e.g., construction defect claims) or a shift in the mixture between smaller, more routine

claims and larger, more complex claims. The Company has reviewed the historical variation in reported loss development patterns. If

the reported loss development patterns change by 9%, the estimated net reserve need would change by $200, in either direction. A 9%

change in reported loss development patterns is within the Company’ s historical variation, as measured by the variation around the

average development factors as reported in statutory accident year reports.

Similar to general liability, assumed casualty reinsurance is affected by reported loss development patterns. In addition to the items

identified above that would affect both direct and reinsurance liability claim development patterns, there is also an impact to reporting

patterns for any changes in claim notification from ceding companies to the reinsurer. Recorded net reserves for HartRe assumed

reinsurance business, excluding asbestos and environmental liabilities, within Property & Casualty Other Operations were $349 as of

December 31, 2011. If the reported loss development patterns underlying the Company's net reserves for HartRe assumed casualty

reinsurance change by 5%, the estimated net reserve need would change by approximately $95, in either direction. A 5% change in

reported loss development patterns is within the Company’ s historical variation, as measured by the variation around the average

development factors as reported in statutory accident year reports.