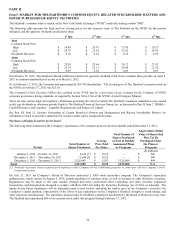

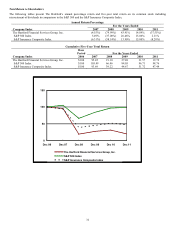

The Hartford 2011 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

40

Reinsurance recoverables include an estimate of the amount of gross loss and loss adjustment expense reserves that may be ceded under

the terms of the reinsurance agreements, including IBNR unpaid losses. The Company calculates its ceded reinsurance projection based

on the terms of any applicable facultative and treaty reinsurance, often including an estimate by reinsurance agreement of how IBNR

losses will ultimately be ceded.

The Company provides an allowance for uncollectible reinsurance, reflecting management’ s best estimate of reinsurance cessions that

may be uncollectible in the future due to reinsurers’ unwillingness or inability to pay. The Company analyzes recent developments in

commutation activity between reinsurers and cedants, recent trends in arbitration and litigation outcomes in disputes between reinsurers

and cedants and the overall credit quality of the Company’ s reinsurers. Where its contracts permit, the Company secures future claim

obligations with various forms of collateral, including irrevocable letters of credit, secured trusts, funds held accounts and group-wide

offsets. The allowance for uncollectible reinsurance was $290 as of December 31, 2011, including $83 related to Property & Casualty

Commercial and $207 related to Property & Casualty Other Operations.

The Company’ s estimate of reinsurance recoverables, net of an allowance for uncollectible reinsurance, is subject to similar risks and

uncertainties as the estimate of the gross reserve for unpaid losses and loss adjustment expenses.

The Hartford, like other insurance companies, categorizes and tracks its insurance reserves for its segments by “line of business”.

Furthermore, The Hartford regularly reviews the appropriateness of reserve levels at the line of business level, taking into consideration

the variety of trends that impact the ultimate settlement of claims for the subsets of claims in each particular line of business. In

addition, Property & Casualty Other Operations categorizes reserves as asbestos and environmental (“A&E”), whereby the Company

reviews these reserve levels by type of event, rather than by line of business. Adjustments to previously established reserves, which

may be material, are reflected in the operating results of the period in which the adjustment is determined to be necessary. In the

judgment of management, information currently available has been properly considered in the reserves established for losses and loss

adjustment expenses.

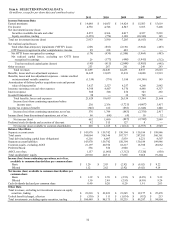

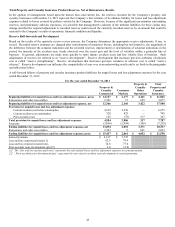

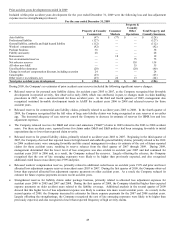

The following table shows loss and loss adjustment expense reserves by line of business as of December 31, 2011, net of reinsurance:

Property & Casualty

Commercial

Consumer

Markets

Property & Casualty

Other Operations

Total Property and

Casualty Insurance

Reserve Line of Business

Commercial property

$

187

$

—

$

—

$

187

Homeowners’

—

467

—

467

Auto physical damage

16

29

—

45

Auto liability

564

1,523

—

2,087

Package business

1,282

—

— 1,282

Workers’ compensation

7,471

—

—

7,471

General liability

2,641

31

—

2,672

Professional liability

702

—

—

702

Fidelity and surety

210

—

—

210

Assumed reinsurance

—

—

349

349

All other non-A&E

—

—

810

810

A&E

21

2

2,212

2,235

Total reserves-net

13,094

2,052

3,371

18,517

Reinsurance and other recoverables

2,343

9

681

3,033

Total reserves-gross

$

15,437

$

2,061

$

4,052

$

21,550

Reserving Methodology

(See Reserving for Asbestos and Environmental Claims within Property & Casualty Other Operations for a discussion of how

A&E reserves are set)

How reserves are set

Reserves are set by line of business within the various segments. A single line of business may be written in more than one segment.

Case reserves are established by a claims handler on each individual claim and are adjusted as new information becomes known during

the course of handling the claim. Lines of business for which loss data (e.g., paid losses and case reserves) emerge (i.e., is reported)

over a long period of time are referred to as long-tail lines of business. Lines of business for which loss data emerge more quickly are

referred to as short-tail lines of business. The Company’ s shortest-tail lines of business are property and auto physical damage. The

longest tail lines of business include workers’ compensation, general liability, professional liability and assumed reinsurance. For short-

tail lines of business, emergence of paid loss and case reserves is credible and likely indicative of ultimate losses. For long-tail lines of

business, emergence of paid losses and case reserves is less credible in the early periods and, accordingly, may not be indicative of

ultimate losses.