HSBC 2002 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

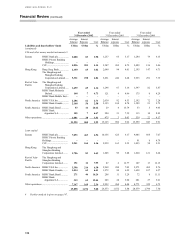

Financial Review (continued)

96

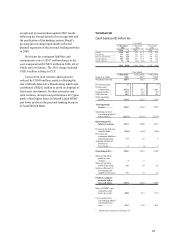

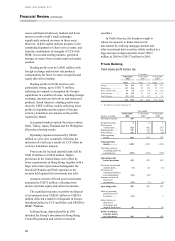

segment including the impact of the Princeton Note

provision and exceptional bad debt provisions and

currency redenomination losses in Argentina.

Net fees and commissions and other income of

the Group’ s wholesale insurance operations

amounted to US$297 million in 2001 and US$256

million in 2000.

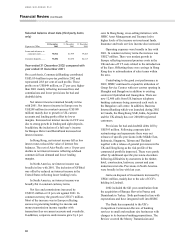

Critical Accounting Policies

Introduction

The results of HSBC Holdings plc are sensitive to

the accounting policies, assumptions and estimates

that underlie the preparation of its consolidated

financial statements. The accounting policies used in

the preparation of the consolidated financial

statements are set out in Note 2 in the ‘Notes to the

financial statements’ on pages 197 to 202.

When preparing the financial statements, it is the

directors’ responsibility under UK company law to

select suitable accounting policies and to make

judgements and estimates that are reasonable and

prudent. Under UK GAAP, Financial Reporting

Standard 18 ‘Accounting Policies’ requires the

Group to adopt the most appropriate accounting

policies in order to give a true and fair view.

HSBC also provides details of its net income

and shareholders’ equity calculated in accordance

with US GAAP. US GAAP differs in certain

respects from UK GAAP. Details of these

differences are set out in Note 50 to the financial

statements on pages 286 to 313.

The accounting policies that are deemed critical

to the Group’s results and financial position, based

upon materiality and significant judgement and

estimates, are discussed below.

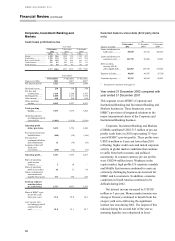

Provisions for bad and doubtful debts

HSBC’s accounting policy for provisions for bad and

doubtful debts on customer loans is described in

Note 2 (b) to the financial statements on pages 197 to

199. The process for applying this policy is described

on pages 122 to 124.

Specific provisions

Specific provisions are established either on a case-

by-case basis or on a portfolio basis, depending on

the nature of the asset. In addition, provisions for the

sovereign risk inherent in cross-border credit

exposures are established for certain countries; this

element is not currently significant.

Where specific provisions are established on a

case-by-case basis, the most important factors are:

• the amount and timing of cashflows forecast to

be received from the borrower; and

• the enforceability and amount which may be

recovered through the sale of any security held.

In many cases, the determination of these factors

will be judgmental, either because the security may

not be readily marketable or the cashflows will

require an assessment of the customer’ s future

performance. HSBC’ s practice is to make a

conservative estimate of these factors and to review

and update them on a regular basis.

This basis of determining provisions is applied

to residential mortgages more than 90 days

delinquent and to most corporate loans. Corporate

loans and residential mortgages together comprise

about 85 per cent of loans and advances to non-

financial customers.

HSBC has no individual loans for which specific

bad and doubtful debt provisions have been

established on a case-by-case basis where changes in

the underlying factors could cause a material change

to the Group’ s reported results.

Where specific provisions are raised on a

portfolio basis, the most important factors are:

• loss rate set for each delinquency category;

• roll rates where determined for specific

portfolios; and

• the period embedded in the loss rate and roll rate

calculations which is designed to reflect only

losses inherent at the reporting date and not

future losses.

The factor most susceptible to variability in

management judgement is the period used in the loss

rate and roll rate calculations. This factor is kept

under continuous review based on the incidence of

losses experienced.

The portfolio basis is applied to small corporate

accounts (typically less than US$15,000) in certain

countries, residential mortgages overdue but less

than 90 days overdue, credit card and other