HSBC 2002 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

163

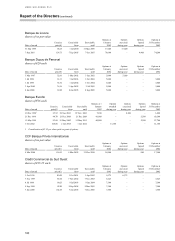

Internal control

The Directors are responsible for internal control in

HSBC and for reviewing its effectiveness.

Procedures have been designed for safeguarding

assets against unauthorised use or disposition; for

maintaining proper accounting records; and for the

reliability of financial information used within the

business or for publication. Such procedures are

designed to manage rather than eliminate the risk

of failure to achieve business objectives and can

only provide reasonable and not absolute assurance

against material errors, losses or fraud. The

procedures also enable HSBC Holdings to

discharge its obligations under the Handbook of

Rules and Guidance issued by the Financial

Services Authority, HSBC’ s lead regulator.

The key procedures that the Directors have

established are designed to provide effective

internal control within HSBC and accord with the

Internal Control Guidance for Directors on the

Combined Code issued by the Institute of

Chartered Accountants in England and Wales.

Such procedures have been in place throughout the

year and up to 3 March 2003, the date of approval

of the Annual Report and Accounts. In the case of

companies acquired during the year, including GF

Bital, the internal controls in place are being

reviewed against HSBC’ s benchmarks and they are

being integrated into HSBC’ s systems. HSBC’ s

key internal control procedures include the

following:

• Authority to operate the various subsidiaries is

delegated to their respective chief executive

officers within limits set by the Board of

Directors of HSBC Holdings or by the Group

Executive Committee under powers delegated

by the Board. Sub-delegation of authority from

the Group Executive Committee to individuals

requires these individuals, within their

respective delegation, to maintain a clear and

appropriate apportionment of significant

responsibilities and to oversee the

establishment and maintenance of systems of

controls appropriate to the business. The

appointment of executives to the most senior

positions within HSBC requires the approval

of the Board of Directors of HSBC Holdings.

• Functional, operating, financial reporting and

certain management reporting standards are

established by Group Head Office

management for application across the whole

of HSBC. These are supplemented by

operating standards set by the local

management as required for the type of

business and geographical location of each

subsidiary.

• Systems and procedures are in place in HSBC

to identify, control and report on the major

risks including credit, changes in the market

prices of financial instruments, liquidity,

operational error, unauthorised activities and

fraud. Exposure to these risks is monitored by

asset and liability committees and executive

committees in subsidiaries and by the Group

Executive Committee for HSBC as a whole.

• Comprehensive annual financial plans are

prepared by subsidiaries and are reviewed and

approved at Group Head Office. Results are

monitored regularly and reports on progress as

compared with the related plan are prepared

throughout HSBC each quarter. A strategic

plan is prepared by major operating

subsidiaries every three years.

• Centralised functional control is exercised

over all computer system developments and

operations. Common systems are employed

where possible for similar business processes.

Credit and market risks are measured and

reported on in subsidiaries and aggregated for

review of risk concentrations on a group-wide

basis.

• Responsibilities for financial performance

against plans and for capital expenditure,

credit exposures and market risk exposures are

delegated with limits to line management in

the subsidiaries. In addition, functional

management in Group Head Office has been

given responsibility to set policies, procedures

and standards in the areas of finance; legal and

regulatory compliance; internal audit; human

resources; credit; market risk; operational risk;

computer systems and operations; property

management; and for certain global product

lines.

• Policies and procedures to guide subsidiary

companies and management at all levels in the