HSBC 2002 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

116

Such audits include consideration of the

completeness and adequacy of credit manuals and

lending guidelines, together with an in-depth analysis

of a representative sample of accounts in the

portfolio to assess the quality of the loan book and

other exposures. Individual accounts are reviewed to

ensure that the facility grade is appropriate, that

credit procedures have been properly followed and

that where an account is non-performing, provisions

raised are adequate. Internal Audit will discuss any

facility grading they consider should be revised at

the end of the audit and their subsequent

recommendations for revised grades must then be

assigned to the facility.

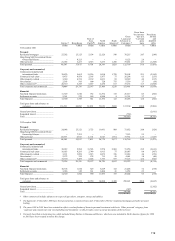

Loan portfolio

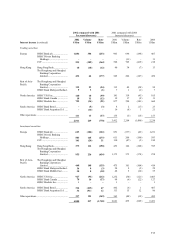

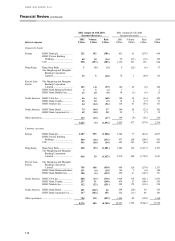

Loans and advances to customers are spread across

the various industrial sectors, as well as

geographically.

At constant exchange rates, loans and advances

to customers (excluding the finance sector and

settlement accounts) grew by US$31.5 billion, or

10.7 per cent during 2002 of which US$9.7 billion,

or 3.2 per cent, related to the acquisition of GFBital

in Mexico. Excluding the impact of GFBital,

personal lending grew by 14.9 per cent and loans and

advances to the commercial and corporate customer

base grew by 1.6 per cent.

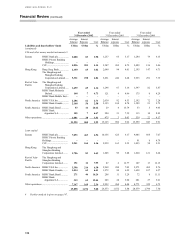

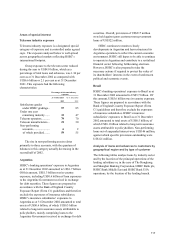

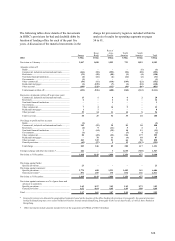

Figures in US$m 2001

Exchange

variance

Under-

lying

change

GF

Bital 2002

Personal:

Residential mortgages 78,215 3,339 14,227 1,203 96,984

Hong Kong SAR

Government

Home Ownership

Scheme ................. 8,123 (1 ) (867 ) – 7,255

Other personal............ 39,125 2,101 6,142 1,194 48,562

Total personal............. 125,463 5,439 19,502 2,397 152,801

Corporate and

commercial:

Commercial,

industrial and

international trade . 70,158 5,219 1,953 1,685 79,015

Commercial real

estate .................... 26,315 1,471 1,394 87 29,267

Other property-related 14,594 519 (17 ) 251 15,347

Government ............... 5,339 (37 ) (476 ) 4,127 8,953

Other commercial....... 37,265 2,812 (292) 889 40,674

Total Corporate and

commercial........... 153,671 9,984 2,562 7,039 173,256

Financial:

Non-bank financial

institutions ............ 26,473 1,473 (733 ) 274 27,487

Settlement accounts.... 11,761 260 (3,636 ) – 8,385

Total financial............ 38,234 1,733 (4,369 )274 35,872

Total gross loans and

advances to

customers.............. 317,368 17,156 17,695 9,710 361,929

The commentary below excludes the impact of

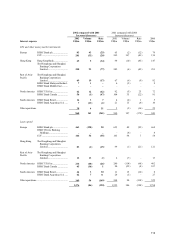

foreign exchange transaction movements and the

acquisition of GFBital except where stated.

Residential mortgages increased by US$14.2

billion, or 18 per cent and including GFBital

comprised 26.8 per cent of total gross loans to

customers at 31 December 2002. Residential

mortgages in Europe increased by US$8.2 billion of

which US$8.0 billion arose in UK Banking as market

initiatives, including First Direct’s smart mortgage,

and competitive pricing resulted in improved

mortgage retention rates and increased share of the

remortgage market. Residential mortgage lending in

Hong Kong was slightly higher than 2001 against a

background of intense mortgage price competition as

HSBC increased its share of the remortgaging

market. This growth was more than offset by a

reduction in loans made under the Hong Kong SAR

Government Home Ownership Scheme (‘GHOS’ ).

At US$7.3 billion residential mortgage loans under

GHOS were US$0.9 billion lower than at 31

December 2001 and resulted from the suspension of

the sale of new homes under this scheme by the

Hong Hong SAR Government in the second half of

2001. In the rest of Asia-Pacific, residential

mortgages grew by US$2.1 billion with strong

growth in Singapore, Malaysia, South Korea, India

and Taiwan. In North America, residential mortgage

lending grew strongly by US$3.3 billion due to

strong mortgage origination as interest rates

remained low.

Including GFBital other personal lending

increased to approximately 13.4 per cent of total

gross loans to customers. Personal lending grew by

US$3.2 billion in Europe. Strong organic growth

was achieved in consumer lending in the UK with an

increase of 10 per cent in credit card advances at 31

December 2002.

Corporate commercial lending grew modestly,

less than 2 per cent, reflecting muted corporate loan

demand and cautious risk appetite.