HSBC 2002 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

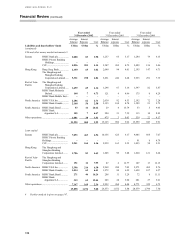

Financial Review (continued)

98

established on the basis of management’s judgement.

Where management’ s judgement is that the

expected cashflows of an IGU have declined and/or

that its cost of capital has increased, the effect will be

to reduce the estimated fair value of the IGU. If this

results in a fair value that is lower than the carrying

value of the IGU, an impairment of goodwill will be

recorded.

Valuation of unquoted and illiquid debt and

equity securities

HSBC’s accounting policy for these instruments is

described in Note 2 (c) on page 199 of the financial

statements.

HSBC carries its debt and equity securities held

for trading purposes at fair value. For those debt and

equity securities which are not carried at fair value,

the fair value of the security is taken into

consideration in determining whether the asset

should be written down to reflect a permanent

impairment.

The fair value determined for unquoted and

illiquid debt and equity securities reflects

management’s assessment of the value of these

securities. This assessment may be based upon the

use of a discounted cashflow model (particularly for

debt securities) or determined by looking directly at

the valuation of comparable securities for which an

independent price can be established.

The main factors which management consider

when applying a cashflow model are:

• the likelihood and expected timing of future

cashflows on the instrument. These cashflows

are usually determined by the terms of the

instrument, although management judgement

may be required in situations where the ability

of the counterparty to service the instrument in

accordance with its contractual terms is in

doubt; and

• an appropriate discount rate for the instrument.

Again management determines this rate, based

on its assessment of the appropriate spread of

the rate for the instrument over the risk free rate.

Where management values the instrument by

reference to comparable securities, the basis of

valuation takes account of the maturity, structure and

rating of the security to which the position held is

being compared.

In assessing the valuation of securities,

management also takes account of the size of the

position held relative to market liquidity and

conditions. Where considered appropriate, the

assessed fair value of the securities will be reduced

to reflect the amount which management estimate

could be realised on their sale.

Changes in any of the assumptions used by

management to determine the valuation will give rise

to changes in the recorded fair value of unquoted

securities. Such changes will result in changes in the

carrying value of the securities where they are

carried at fair value. Where the securities are carried

at amortised cost, changes in their estimated fair

value, arising from changes in management’ s

assumptions on the above variables, may result in the

recording of a permanent diminution in their value.

In this case, it will also be necessary for HSBC’ s

management to exercise judgement as to whether or

not changes in the underlying valuation assumptions

are only temporary.

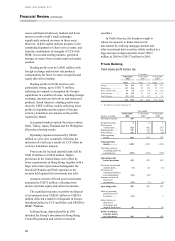

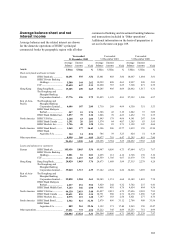

UK GAAP compared with US GAAP

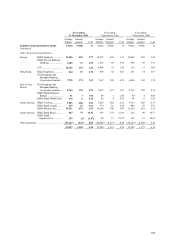

Figures in US$m 2002 2001 2000

Net income:

US GAAP................... 4,900 4,911 6,236

UK GAAP .................. 6,239 4,992 6,457

Shareholder’ s equity:

US GAAP................... 55,831 48,444 48,072

UK GAAP .................. 52,406 46,388 46,393

Differences result from the different treatment of

lease financing, shareholders’ interest in the long-

term assurance fund, pension costs, stock-based

compensation, goodwill, internal software costs,

revaluation of property, purchase accounting

adjustments, accruals accounted derivatives,

permanent diminution in value of available-for-sale

securities, foreign exchange gains on investment

securities, foreign exchange losses on Argentine

funding, fair value adjustment for securities

available-for-sale, dividends payable, own shares

held and deferred taxation. See Note 50 of the ‘Notes

on the Financial Statements’ .

Future accounting developments

The Accounting Standards Board (UK GAAP) and