HSBC 2002 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

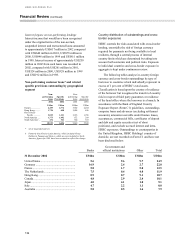

139

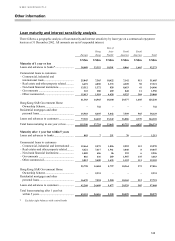

Where considered appropriate, treasury units

and ALCO may use a variety of instruments to

manage interest rate risk, for example to lengthen or

to shorten the duration of the interest risk position.

The range of permitted instruments varies by

location, but is generally restricted to on-balance

sheet financial instruments and plain vanilla interest

rate swaps.

In addition, in the second half of 2002, in

response to the low level of interest rates in the Asian

bloc, ALCO approved the purchase of an interest rate

floor to reduce the effect of further interest rate cuts

to interest margins. The effect of the floor is included

in the sensitivity tables shown below.

Assuming no management action in response to

interest rate movements, an immediate hypothetical

100 basis points parallel fall in all yield curves

worldwide on 1 January 2003 would decrease

planned net interest income for the 12 months to 31

December 2003 by US$690 million while a

hypothetical 100 basis points parallel rise in all yield

curves would decrease planned net interest income

by US$252 million.

Rather than assuming that all interest rates move

together, HSBC’s interest rate exposures can be

grouped into currency blocs whose interest rates are

considered more likely to move together. The

sensitivity of net interest income for 2003 can then

be described as follows:

Figures in US$ m

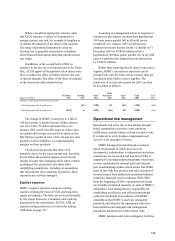

US dollar

bloc

Sterling

bloc

Asian

bloc

Latin

American

bloc

Euro

bloc

Total

2003

Total

2002

Change in 2003 projected net interest income

+100 basis points shift in yield curves

–

(

47)

(

225)69

(

49)

(

252)(200)

−100 basis points shift in yield curves

(

243)6

(

437)

(

66)50

(

690)(196)

The change in HSBC’s sensitivity to a fall of

100 basis points is mainly because further interest

rate cuts in the US dollar and Asian blocs at 1

January 2003 would not offer scope to reduce rates

on current and savings accounts by as much as the

full 100 basis points in view of the already low rates

payable on these liabilities, so compressing the

margins on these products.

The projections assume that rates of all

maturities move by the same amount and, therefore,

do not reflect the potential impact on net interest

income of some rates changing while others remain

unchanged. The projections also make other

simplifying assumptions, including an assumption

that all positions run to maturity. In practice, these

exposures are actively managed.

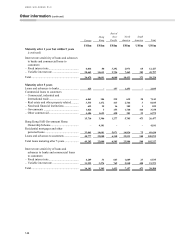

Equities exposure

HSBC’s equities exposure comprises trading

equities, forming the basis of VAR, and long-term

equity investments. The latter are reviewed annually

by the Group Executive Committee and regularly

monitored by the subsidiaries’ ALCOs. VAR on

equities trading positions is set out in the trading

VAR table on page 137.

Operational risk management

Operational risk is the risk of loss arising through

fraud, unauthorised activities, error, omission,

inefficiency, systems failure or from external events.

It is inherent to every business organisation and

covers a wide spectrum of issues.

HSBC manages this risk through a controls-

based environment in which processes are

documented, authorisation is independent and where

transactions are reconciled and monitored. This is

supported by an independent programme of periodic

reviews undertaken by internal audit and internal

peer benchmarking studies which ensure that HSBC

stays in line with best practice and takes account of

lessons learned from publicised operational failures

within the financial services industry. With effect

from the beginning of 2001, operational risk losses

are formally monitored quarterly. In each of HSBC’s

subsidiaries local management is responsible for

establishing an effective and efficient operational

control environment in accordance with HSBC

standards so that HSBC’s assets are adequately

protected, and whereby the operational risks have

been identified and adequate risk management

procedures maintained to control those risks.

HSBC maintains and tests contingency facilities