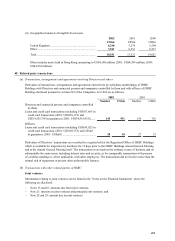

HSBC 2002 Annual Report Download - page 289

Download and view the complete annual report

Please find page 289 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

287

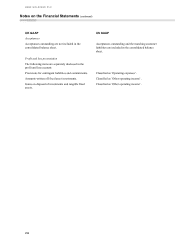

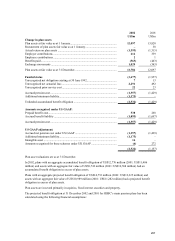

UK GAAP US GAAP

Pension costs

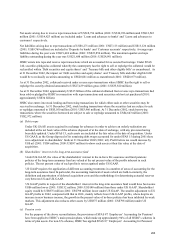

Pension costs, based on actuarial assumptions and

methods, are charged so as to allocate the cost of

providing benefits over the average remaining service

lives of employees.

SFAS 87 ‘Employers’ Accounting for Pensions’

prescribes a similar method of actuarial valuation but

requires assets to be assessed at fair value and the

assessment of liabilities to be based on current

settlement rates. Certain variations from regular cost

are allocated in equal amounts over the average

remaining service lives of current employees.

Stock-based compensation

For executive share option schemes, such options are

granted at fair value and no compensation costs are

recognised under the ‘intrinsic value method’ .

For Save-As-You-Earn schemes, employees are

granted shares at a 20 per cent discount to fair value at

the date of grant. No compensation cost is recognised

for such awards.

SFAS 123 ‘Accounting for Stock Based

Compensation’ encourages a fair value based method

of accounting for stock-based compensation plans.

Under the fair value method, compensation cost is

measured at date of grant based on the value of the

award and its recognised over the service period, which

is usually the vesting period. Where options lapse

before their costs have been fully recognised, any costs

previously recognised relating to lapsed options are

written back.

For longer term and other restricted share award

schemes, the fair value of the shares awarded is

charged to compensation cost over the period in respect

of which performance conditions apply. To the extent

the award is adjusted by virtue of performance

conditions being met or not, the compensation cost is

adjusted in line with this.

Goodwill

For acquisitions prior to 1998, goodwill arising on the

acquisition of subsidiary undertakings, associates or

joint ventures was charged against reserves in the year

of acquisition.

Goodwill acquired up to 30 June 2001was capitalised

and amortised over its estimated useful life but not

more than 25 years. Goodwill acquired after 30 June

2001 is not amortised. Previously acquired goodwill

ceased to be amortised from 31 December 2001.

For acquisitions made on or after 1 January 1998,

goodwill is included in the balance sheet and amortised

over its estimated useful life on a straight-line basis.

UK GAAP allows goodwill previously eliminated

against reserves to be reinstated, but does not require it.

In common with many other UK companies, HSBC

elected not to reinstate such goodwill. HSBC

considered whether reinstatement would materially

assist the understanding of readers of its accounts who

were already familiar with UK GAAP and decided that

it would not.

SFAS 142 ‘Goodwill and Other Intangible Assets’

requires that goodwill should not be amortised but

should be tested for impairment at least annually at the

reporting unit level by applying a fair-value-based test.