HSBC 2002 Annual Report Download - page 197

Download and view the complete annual report

Please find page 197 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements

195

1 Basis of preparation

(a) The financial statements have been prepared under the historical cost convention, as modified by the revaluation

of certain investments and land and buildings, and in accordance with applicable accounting standards.

The consolidated financial statements are prepared in accordance with the special provisions of Part VII Chapter

II of the UK Companies Act 1985 (‘the Act’ ) relating to banking groups. The consolidated financial statements

comply with Schedule 9 and the financial statements of HSBC Holdings comply with Schedule 4 to the Act.

As permitted by Section 230 of the Act, no profit and loss account is presented for HSBC Holdings.

HSBC has adopted the provisions of the UK Financial Reporting Standard (‘FRS’ ) FRS 19 ‘Deferred Tax’ with

effect from 1 January 2002, and the transitional arrangements of FRS 17 ‘Retirement benefits’ , which require

additional disclosures only. For a discussion of the impact of the adoption of FRS 19 see Note 1(e) below.

The accounts have been prepared in accordance with the Statements of Recommended Accounting Practice

(‘SORPs’ ) issued by the British Bankers’ Association (‘BBA’ ) and Irish Bankers’ Federation (‘IBF’ ) and with

the SORP ‘Accounting issues in the asset finance and leasing industry’ issued by the Finance & Leasing

Association (‘FLA’ ).

The SORP issued by the Association of British Insurers (‘ABI’ ) ‘Accounting for insurance business’ contains

recommendations on accounting for insurance business for insurance companies and insurance groups. HSBC is

primarily a banking group, rather than an insurance group, and, consistent with previously established practice

for such groups preparing consolidated financial statements complying with Schedule 9 to the Act, values its

long-term assurance businesses using the Embedded Value method. This method includes a prudent valuation of

the discounted future earnings expected to emerge from business currently in force, taking into account factors

such as recent experience and general economic conditions, together with the surplus retained in the long-term

assurance funds.

(b) The preparation of financial information requires the use of estimates and assumptions about future conditions.

In this connection, management believes that the critical accounting policies are those in relation to provisions

for bad and doubtful debts, goodwill impairment, and the valuation of unquoted and illiquid debt and equity

securities. Application of these policies and the key estimates and assumptions used are described in the

Financial Review section on pages 96 to 98 under the heading ‘Critical Accounting Policies’ .

(c) The consolidated financial statements of HSBC comprise the financial statements of HSBC Holdings and its

subsidiary undertakings. Financial statements of subsidiary undertakings are made up to 31 December. In the

case of the principal banking and insurance subsidiaries of HSBC Bank Argentina, whose financial statements

are made up to 30 June annually to comply with local regulations, HSBC uses audited interim financial

statements, drawn up to 31 December annually. The consolidated financial statements include the attributable

share of the results and reserves of joint ventures and associates, based on financial statements made up to dates

not earlier than six months prior to 31 December.

All significant intra-HSBC transactions are eliminated on consolidation.

(d) HSBC’ s financial statements are prepared in accordance with UK generally accepted accounting principles

(‘UK GAAP’ ), which differ in certain respects from US generally accepted accounting principles (‘US GAAP’ ).

For a discussion of significant differences between UK GAAP and US GAAP and a reconciliation to US GAAP

of certain amounts see Note 50. In addition, certain disclosures in the Notes on the Financial Statements have

been made to comply with US reporting requirements.

(e) The adoption of FRS 19 has required a change in the method of accounting for deferred tax. Deferred tax is now

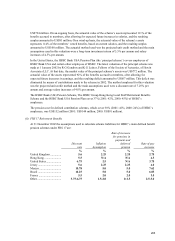

recognised in full, subject to recoverability of deferred tax assets. Previously, deferred tax assets and liabilities

were recognised only to the extent they were expected to crystallise. As deferred tax liabilities have generally

been fully provided, the main impact of the change in method for HSBC has been the recognition of deferred tax

assets previously not recognised. The change in accounting policy has been reflected by way of a prior period

adjustment. The comparative figures have been restated as follows: