HSBC 2002 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

51

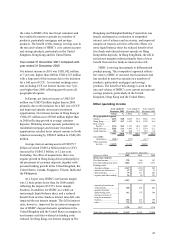

US$408 million (2001: US$450 million) provided at

a rate of 16 per cent (2001: 16 per cent) on the profits

assessable in Hong Kong. Other overseas taxation

was provided for in the countries of operation at the

appropriate rates of taxation.

HSBC’s effective tax rate of 26.3 per cent in

2002 was higher than that for 2001 (24.9 per cent)

mainly as a result of the geographic mix of profits

and certain non-recurring items which occurred in

2001 and resulted in a reduction in the 2001 rate.

In particular, profits arising in North America

represented a higher percentage of HSBC’s profits in

2002 compared to 2001 because profits in the US

were abnormally suppressed in 2001 by the provision

relating to the Princeton Note settlement. US profits

are taxed at a higher rate than the average for the rest

of the group and thus this change in mix raised the

overall tax rate of the group.

One-off tax-free gains arising in 2002 were less

than those arising in 2001.

Partly offsetting these factors, no tax relief was

assumed in respect of the bad debt provision and

other losses relating to Argentina. These losses and

provisions were lower in 2002 than in 2001. This had

the effect of increasing the aggregate tax rate in both

2002 and 2001 but by a lesser degree in 2002.

In 2002, prior year adjustments mainly relating

to audit settlements, which resulted in a reduction in

the tax rate, were less than similar adjustments in

2001.

At 31 December 2002 there were potential

future tax benefits of US$885 million (2001: US$906

million) in respect of trading losses, allowable

expenditure charged to the profit and loss account

but not yet allowable for tax, and capital losses

which had not yet been recognised because

realisation of the benefits was not considered certain.

Year ended 31 December 2001 compared to

year ended 31 December 2000

HSBC Holdings and its subsidiary undertakings in

the United Kingdom provided for UK corporation

tax at 30 per cent, the rate for the calendar year 2001

(2000: 30 per cent).

Overseas tax included Hong Kong profits tax of

US$450 million (2000: US$478 million) provided at

a rate of 16 per cent (2000: 16 per cent) on the profits

assessable in Hong Kong. Other overseas taxation

was provided for in the countries of operation at the

appropriate rates of taxation.

HSBC’s effective tax rate of 24.9 per cent in

2001 was in line with that for 2000 (24.6 per cent)

although there were several factors either increasing

or reducing the rate.

Profits arising in North America represented a

lower percentage of HSBC’s profits in 2001

compared to 2000 because the profits in the US were

suppressed in 2001 by the provision relating to the

Princeton Note settlement. Because these profits are

taxed at a higher rate than the average for the rest of

the group this reduces the overall group tax rate in

2001.

One-off tax-free gains arose in 2001 and these

were greater than those arising in 2000.

No tax relief has been assumed for the 2001 bad

debt provision relating to Argentina. This increases

the 2001 tax rate.

In 2001 certain prior year adjustments mainly

relating to audit settlements resulted in a reduction in

the tax rate. There were similar adjustments in 2001

which resulted in a lower reduction in the tax rate.

At 31 December 2001 there were potential

future tax benefits of US$906m (2000: US$350m) in

respect of trading losses, allowable expenditure

charged to the profit and loss account but not yet

allowable for tax and capital losses which have not

yet been recognised because realisation of the

benefits is not considered certain.