HSBC 2002 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

198

Specific provisions

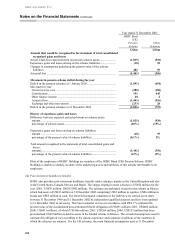

Specific provisions represent the quantification of actual and expected losses from identified accounts and are

deducted from loans and advances in the balance sheet.

Other than where provisions on smaller balance homogenous loans are assessed on a portfolio basis, the amount

of specific provision raised is assessed on a case by case basis. The amount of specific provision raised is HSBC’ s

conservative estimate of the amount needed to reduce the carrying value of the asset to the expected ultimate net

realisable value, and in reaching a decision consideration is given, among other things, to the following factors:

− the financial standing of the customer, including a realistic assessment of the likelihood of repayment of the

loan within an acceptable period and the extent of HSBC’ s other commitments to the same customer;

− the realisable value of any security for the loan;

− the costs associated with obtaining repayment and realisation of the security; and

− if loans are not in local currency, the ability of the borrower to obtain the relevant foreign currency.

Where specific provisions are raised on a portfolio basis, the level of provisioning takes into account

management’ s assessment of the portfolio's structure, past and expected credit losses, business and economic

conditions, and any other relevant factors. The principal portfolios evaluated on this basis are credit cards and

other consumer lending products.

General provisions

General provisions augment specific provisions and provide cover for loans which are impaired at the balance

sheet date but which will not be identified as such until some time in the future. HSBC requires operating

companies to maintain a general provision which is determined taking into account the structure and risk

characteristics of each company’ s loan portfolio. Historical levels of latent risk are regularly reviewed by each

operating company to determine that the level of general provisioning continues to be appropriate. Where

entities operate in a significantly higher risk environment, an increased level of general provisioning will apply

taking into account local market conditions and economic and political factors. General provisions are deducted

from loans and advances to customers in the balance sheet.

Loans on which interest is being suspended

Provided that there is a realistic prospect of interest being paid at some future date, interest on non-performing

loans is charged to the customer’ s account. However, the interest is not credited to the profit and loss account

but to an interest suspense account in the balance sheet which is netted against the relevant loan. On receipt of

cash (other than from the realisation of security), suspended interest is recovered and taken to the profit and loss

account. A specific provision of the same amount as the interest receipt is then raised against the principal

balance. Amounts received from the realisation of security are applied to the repayment of outstanding

indebtedness, with any surplus used to recover any specific provisions and then suspended interest.

Non-accrual loans

Where the probability of receiving interest payments is remote, interest is no longer accrued and any suspended

interest balance is written off.

Loans are not reclassified as accruing until interest and principal payments are up-to-date and future payments

are reasonably assured.

Loan write-offs

Loans and suspended interest are written off, either partially or in full, when there is no prospect of recovery of

these amounts.

Assets acquired in exchange for advances

Assets acquired in exchange for advances in order to achieve an orderly realisation continue to be reported as