HSBC 2002 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

86

interest income in Europe was effectively flat. In

the UK, the benefit of customer deposit growth was

offset by the impact on margins of competitive

pricing initiatives in mortgages and savings

accounts.

In Hong Kong net interest income rose by

US$41 million as the benefits of increased credit

card lending and wider spreads on non-Hong Kong

dollar lending were largely offset by lower spreads

on Hong Kong Dollar savings and deposit accounts

and on residential mortgages.

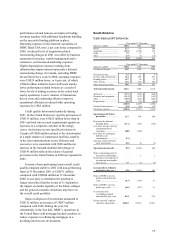

Net interest income for the Rest of Asia-

Pacific rose by US$53 million with encouraging

growth in most entities in the region. In North

America increased net interest income of US$73

million reflected wider margins as funding costs

fell more quickly than lending, particularly

mortgage lending, repriced. The decline in funding

costs was further helped by a switch by depositors

away from fixed rate CDs to lower-paying savings

and current accounts.

Net fees and commissions rose by US$233

million or 9 per cent on the year. US$127 million

of this rise was in Europe, again mainly reflecting

the inclusion of a full year of results for CCF. Fees

in the UK fell slightly as lower overdraft fees and

the effect of removing ATM fees on the LINK

network and mortgage valuation fees were only

partially offset by growth in wealth management

income and fees on investment products. Net fees

in Hong Kong were up by US$76 million, with

outstanding success in fees earned from sales of

capital-guaranteed funds.

In North America fee income was effectively

unchanged; strongly rising wealth management

income and fees from high levels of mortgage

augmentation were offset by increased write-offs of

mortgage servicing rights as mortgage prepayments

rose in response to falling interest rates. The

mortgage business also suffered losses on

instruments held as hedges against the value of

mortgage servicing rights; such losses are reflected

in dealing profits. Overall the mortgage business

generated positive net interest and non-interest

income.

Other income rose by US$95 million,

primarily in Hong Kong due to strong growth in

life insurance income fees and the growth in

embedded value in this business.

Operating expenses increased by US$240

million or 4 per cent, mainly reflecting a US$137

million rise in staff costs and US$43 million of

increased premises and equipment expenses. In

Europe, expenses rose by US$229 million, mainly

due to the inclusion of a full year’ s costs for CCF.

Excluding this increase, costs in Europe were

down. In constant currency terms, the UK bank’s

staff costs rose 4 per cent due to annual pay rises

and increased headcount in wealth management

and customer telephone services.

Costs in Hong Kong increased by US$147

million, reflecting increased marketing and IT

costs, together with the impact of annual salary

increments and expansion of the cards business and

Mandatory Provident Fund services. In the rest of

Asia-Pacific, a US$96 million rise in costs

included increased costs following acquisitions and

branch openings, higher costs associated with the

expansion of wealth management services, costs of

mortgage incentives in Malaysia and branch

expansion in a number of countries.

Operating costs declined by US$66 million in

North America mainly due to the non-recurrence of

restructuring costs associated with the RNYC

acquisition in 2000, partly offset by increased

wealth management expenses together with lower

performance-based salaries in Canada. Costs in

South America were lower by US$165 million,

mainly due to the effect of exchange rate changes

in Brazil. Local currency costs were up slightly in

Brazil, reflecting higher transactional taxes.

Provisions for bad and doubtful debts rose

from US$602 million to US$767 million. In

Europe lower provisions (down by US$58 million),

partly reflected improved recovery procedures in

First Direct and the cards portfolio.

Provisions in Hong Kong rose by US$94

million as the weakening economic environment

led to an increase in personal bankruptcies and this,

together with a rise in card lending, resulted in

increased provisions on credit cards. Provisions in

the Rest of Asia-Pacific rose by US$84 million,

with higher charges in Taiwan and the non-

recurrence of the benefit seen in 2000 from the

release of part of the Asia special general

provision. South American loan losses rose by

US$23 million, including US$11 million in

Argentina due to the economic situation in the

country. South American provisioning excludes the