HSBC 2002 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

61

14 per cent increase in fee income from cards.

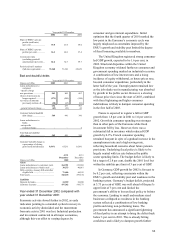

In Treasury and Capital Markets, other operating

income was US$52 million, or 14 per cent, lower

than 2000. This was primarily due to lower income

in gilts trading, which did not repeat the strong

performance of the first half of 2000 and the costs

associated with the interest rate hedge on the

increased holdings of investment grade corporate

bonds.

In Investment Banking, there were significantly

lower levels of fee income from broking and other-

securities related income as the high market volumes

and favourable stock market movements in the first

half of 2000 were followed by eighteen months of

declining volumes in primary and secondary equity

markets and declines in merger and acquisition

activity. Dealing profits in equity trading business

were also lower as volumes fell sharply, reflecting

the adverse market conditions.

Operating expenses before goodwill

amortisation at US$7,288 million were US$1,023

million, or 16 per cent, higher than in 2000. CCF’s

operating expenses before goodwill amortisation

were US$1,441 million (2000: US$674 million for

five months) in 2001. Excluding CCF, operating

expenses before goodwill amortisation at US$5,847

million were US$256 million higher than 2000.

About a third of this related to increased information

technology-related expenditure.

CCF operating costs of US$1,441 million (2000:

US$674 million for five months) reflected a full year

trading period and the acquisition of Banque Hervet,

together with strict cost control. Excluding changes

in corporate structure and on a full year basis,

operating costs increased by only 1.7 per cent,

mainly from non-recurring expenses.

Staff costs at US$4,227 million were US$521

million higher than 2000 (of which US$448 million

related to CCF) . In UK Banking staff costs increased

by 7 per cent to US$1,922 million as staff numbers

were increased to support business development and

higher business volumes, including wealth

management activities and customer telephone

services. Additional IT staff numbers have supported

service improvement projects, particularly relating to

expanding delivery channels including the internet.

Profit-related remuneration reflected the higher

revenues generated in treasury and capital markets,

offset by lower payments as revenues declined in

securities related and corporate finance activities.

Non-staff costs grew by US$502 million (of

which US$302 million related to CCF) to US$3,061

million, including an increase in information

technology-related expenditure and increase in the

cost of services contracted out, primarily relating to

the outsourcing of HSBC Bank plc’s cash and

cheque processing services.

Higher costs in Greece reflected the acquisition

of additional branches and in Turkey of Demirbank.

The charge for bad and doubtful debts was

US$110 million, or 33 per cent, higher at US$441

million. Of this US$81 million was attributable to

CCF. In UK Banking the charge for bad and

doubtful debts was US$57 million, or 15 per cent,

lower than in 2000. New specific provisions,

recoveries and releases were in line with 2000 as

underlying credit quality remained stable. Lower

levels of new specific provisions were raised for

First Direct and on credit card advances but new

provisions for commercial loans were slightly higher

and reflected problems seen in the manufacturing

sector and weakening in business confidence.

In HSBC Republic Suisse, an increase in new

provisions against a corporate exposure in the

Channel Islands was offset by the release of general

provisions. This release reflects the reassessment of

the historical risk factors associated with higher

quality private bank lending.

CCF’s charge for bad and doubtful debts of

US$77 million (2000: US$4 million release for five

months) remains at a moderate level illustrating the

good quality of CCF loan book in spite of some

deterioration in the airline industry.

Provisions for contingent liabilities were US$36

million lower at US$30 million. The 2000

comparative included a charge in UK Banking for

the amount of redress potentially payable to

customers who may have been disadvantaged when

transferring from or opting out of occupational

pension schemes.

Amounts written off fixed asset investments of

US$90 million arose mainly from venture capital

investments and holdings of emerging technology

stocks.

The share of operating losses in joint ventures

primarily reflected HSBC’ s share of losses in Merill

Lynch HSBC’s European operations. The 2000

comparatives for the share of operating losses in

associated undertakings included losses of US$76