Boeing 2005 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2005 Boeing annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

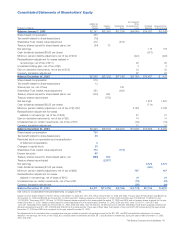

Notes to Consolidated Financial Statements

(Dollars in millions except per share data)

Note 1 - Summary of Significant Accounting Policies

Principles of consolidation

Our consolidated financial statements include the accounts of

all majority-owned subsidiaries and variable interest entities that

are required to be consolidated. The equity method of account-

ing is used for our investments in joint ventures for which we

do not have control or are not the primary beneficiary, but over

whose operating and financial policies we have the ability to

exercise significant influence.

Reclassifications

Certain reclassifications have been made to prior periods to

conform to the current year presentation.

In addition, we have made certain reclassifications to the

Consolidated Statements of Cash Flows primarily due to the

classification of dividends received from equity method

investees and the classification of excess tax benefits from

share-based payment arrangements. We do not feel the effects

are material. The following table provides the net impact of

these reclassifications.

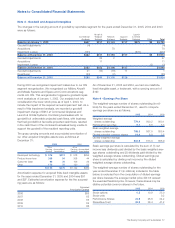

2004 2003

Net impact to operating activities $«46 $67

Net impact to investing activities (77) (52)

Net impact to financing activities 31 (15)

Use of estimates

The preparation of financial statements in conformity with

accounting principles generally accepted in the United States

of America requires management to make assumptions and

estimates that directly affect the amounts reported in the con-

solidated financial statements. Significant estimates for which

changes in the near term are considered reasonably possible

and that may have a material impact on the financial state-

ments are disclosed in these notes to the consolidated financial

statements.

Operating cycle

For classification of current assets and liabilities, we elected to

use the duration of the related contract or program as our

operating cycle which is generally longer than one year and

could exceed 3 years.

Revenue recognition

Contract accounting Contract accounting is used for develop-

ment and production activities predominately by the four seg-

ments within Integrated Defense Systems (IDS). These activities

include the following products and systems: military aircraft,

helicopters, missiles, space systems, missile defense systems,

satellites, rocket engines, and information and battle manage-

ment systems. The majority of business conducted in the IDS

segments is performed under contracts with the U.S.

Government and foreign governments that extend over a num-

ber of years. Contract accounting involves a judgmental

process of estimating the total sales and costs for each con-

tract resulting in the development of estimated cost of sales

percentages. For each contract, the amount reported as cost

of sales is determined by applying the estimated cost of sales

percentage to the amount of revenue recognized.

We combine contracts for accounting purposes when they are

negotiated as a package with an overall profit margin objective;

they essentially represent an agreement to do a single project

for a single customer; they involve interrelated construction

activities with substantial common costs; and they are per-

formed concurrently or sequentially. When a group of contracts

is combined, revenue and profit are earned uniformly over the

performance of the combined contracts.

Sales related to contracts with fixed prices are recognized as

deliveries are made, except for certain fixed-price contracts

that require substantial performance over an extended period

before deliveries begin, for which sales are recorded based on

the attainment of performance milestones. Sales related to

contracts in which we are reimbursed for costs incurred plus

an agreed upon profit are recorded as costs are incurred. The

U.S. Federal Government Acquisition regulations provide guid-

ance on the types of cost that will be reimbursed in establish-

ing contract price. Contracts may contain provisions to earn

incentive and award fees if targets are achieved. Incentive and

award fees that can be reasonably estimated are recorded over

the performance period of the contract. Incentive and award

fees that cannot be reasonably estimated are recorded when

awarded.

Program accounting Our Commercial Airplanes segment uses

program accounting to account for sales and cost of sales

related to all commercial airplane programs. Program account-

ing is a method of accounting applicable to products manufac-

tured for delivery under production-type contracts where

profitability is realized over multiple contracts and years. Under

program accounting, inventoriable production costs, program

tooling costs and routine warranty costs are accumulated and

charged to cost of sales by program instead of by individual

units or contracts. A program consists of the estimated number

of units (accounting quantity) of a product to be produced in a

continuing, long-term production effort for delivery under exist-

ing and anticipated contracts. To establish the relationship of

sales to cost of sales, program accounting requires estimates

of (a) the number of units to be produced and sold in a pro-

gram, (b) the period over which the units can reasonably be

expected to be produced, and (c) the units’ expected sales

prices, production costs, program tooling, and warranty costs

for the total program.

We recognize sales for commercial airplane deliveries as each

unit is completed and accepted by the customer. Sales recog-

nized represent the price negotiated with the customer,

adjusted by an escalation formula. The amount reported as

cost of sales is determined by applying the estimated cost of

sales percentage for the total remaining program to the amount

of sales recognized for airplanes delivered and accepted by the

customer.

50 The Boeing Company and Subsidiaries