Boeing 2005 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2005 Boeing annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

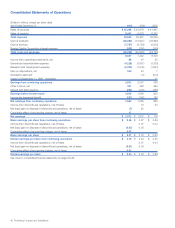

Management’s Discussion and Analysis

Program Accounting

Program accounting requires the demonstrated ability to reli-

ably estimate the relationship of sales to costs for the defined

program accounting quantity. A program consists of the esti-

mated number of units (accounting quantity) of a product to be

produced in a continuing, long-term production effort for deliv-

ery under existing and anticipated contracts. For each pro-

gram, the amount reported as cost of sales is determined by

applying the estimated cost of sales percentage for the total

remaining program to the amount of sales recognized for air-

planes delivered and accepted by the customer.

Factors that must be estimated include program accounting

quantity, sales price, labor and employee benefit costs, material

costs, procured parts, major component costs, overhead costs,

program tooling costs, and routine warranty costs. Underlying

all estimates used for program accounting is the forecasted

market and corresponding production rates. Estimation of the

accounting quantity for each program takes into account sev-

eral factors that are indicative of the demand for the particular

program, such as firm orders, letters of intent from prospective

customers, and market studies. Total estimated program sales

are determined by estimating the model mix and sales price for

all unsold units within the accounting quantity, added together

with the sales for all undelivered units under contract. The sales

prices for all undelivered units within the accounting quantity

include an escalation adjustment that is based on projected

escalation rates, consistent with typical sales contract terms.

Cost estimates are based largely on negotiated and anticipated

contracts with suppliers, historical performance trends, and

business base and other economic projections. Factors that

influence these estimates include production rates, internal and

subcontractor performance trends, asset utilization, anticipated

labor agreements, and inflationary trends.

To ensure reliability in our estimates, we employ a rigorous esti-

mating process that is reviewed and updated on a quarterly

basis. Changes in estimates are recognized on a prospective

basis.

Due to the significance of judgment in the estimation process

described above, it is likely that materially different cost of sales

amounts could be recorded if we used different assumptions,

or if the underlying circumstances were to change. Changes in

underlying assumptions/estimates, or circumstances may

adversely or positively affect financial performance in future

periods.

Our recent experience has been that estimated changes due to

accounting quantity, model mix, escalation, and cost perform-

ance adjustments have resulted in changes over the course of

a year to the combined cost of sales percentages of all com-

mercial airplane programs within a range of plus or minus 1%.

If combined cost of sales percentages for all commercial air-

plane programs for all of 2005 had been estimated to be higher

or lower by 1%, it would have increased or decreased income

for 2005 by approximately $190 million.

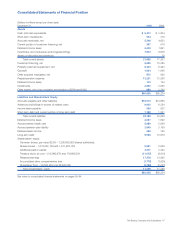

Aircraft Valuation

Used aircraft under trade-in commitments The fair value of

trade-in aircraft is determined using aircraft specific data such

as, model, age and condition, market conditions for specific

aircraft and similar models, and multiple valuation sources. This

process uses our assessment of the market for each trade-in

aircraft, which in most instances begins years before the return

of the aircraft. There are several possible markets to which we

continually pursue opportunities to place used aircraft. These

markets include, but are not limited to, (1) the resale market,

which could potentially include the cost of long-term storage,

(2) the leasing market, with the potential for refurbishment

costs to meet the leasing customer’s requirements, or (3) the

scrap market. Collateral valuation varies significantly depending

on which market we determine is most likely for each aircraft.

On a quarterly basis, we update our valuation analysis based

on the actual activities associated with placing each aircraft into

a market. This quarterly collateral valuation process yields

results that are typically lower than residual value estimates by

independent sources and tends to more accurately reflect

results upon the actual placement of the aircraft.

Based on the best market information available at the time, it is

probable that we would be obligated to perform on trade-in

commitments with net amounts payable to customers totaling

$72 million and $116 million at December 31, 2005 and 2004.

Accounts payable and other liabilities included $22 million and

$25 million at December 31, 2005 and 2004, which represents

the exposure related to these trade-in commitments.

Had the estimate of trade-in value used to calculate our obliga-

tion related to probable trade-in commitments been 10%

higher or lower than our actual assessment, using a measure-

ment date of December 31, 2005, Accounts payable and other

liabilities would have decreased or increased by approximately

$5 million. We continually update our assessment of the likeli-

hood of our trade-in aircraft purchase commitments and con-

tinue to monitor all these commitments for adverse

developments.

Impairment review for assets under operating leases and held

for sale or re-lease When events or circumstances indicate (and

no less than annually), we review the carrying value of all air-

craft and equipment under operating lease and held for sale or

re-lease for potential impairment. We evaluate assets under

operating lease or held for re-lease for impairment when the

expected undiscounted cash flow over the remaining useful life

is less than the carrying value. We use various assumptions

when determining the expected undiscounted cash flow. A key

assumption is the expected future lease rates. We also include

assumptions about lease terms, end of economic life value of

the aircraft or equipment, periods in which the asset may be

held in preparation for a follow-on lease, maintenance costs,

remarketing costs and the remaining economic life of the asset

and estimated proceeds from future asset sales. We state

assets held for sale at the lower of carrying value or fair value

less costs to sell.

The Boeing Company and Subsidiaries 41