Xerox 2006 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2006 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

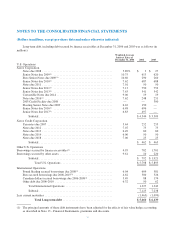

|

|

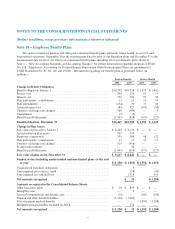

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in millions, except per-share data and unless otherwise indicated)

do not qualify for hedge accounting but are effective as

economic hedges of our inventory purchases and currency

exposure. These derivative contracts are accounted for

using the mark-to-market accounting method and

accordingly are exposed to some level of volatility. Under

this method, the contracts are carried at their fair value on

our consolidated balance sheet within Other assets and

Other liabilities. The level of volatility will vary with the

type and amount of derivative hedges outstanding, as well

as fluctuations in the currency and interest rate market

during the period. The related cash flow impacts of all of

our derivative activities are reflected as cash flows from

operating activities.

We enter into limited types of derivative contracts,

including interest rate and cross currency interest rate

swap agreements, foreign currency spot, forward and

swap contracts and net purchased foreign currency

options to manage interest rate and foreign currency

exposures. Our primary foreign currency market

exposures include the Japanese Yen, Euro, British pound

sterling, Canadian dollar and Brazilian real. The fair

market values of all our derivative contracts change with

fluctuations in interest rates and/or currency rates and are

designed so that any changes in their values are offset by

changes in the values of the underlying exposures.

Derivative financial instruments are held solely as risk

management tools and not for trading or speculative

purposes.

By their nature, all derivative instruments involve, to

varying degrees, elements of market and credit risk not

recognized in our financial statements. The market risk

associated with these instruments resulting from currency

exchange and interest rate movements is expected to

offset the market risk of the underlying transactions,

assets and liabilities being hedged. We do not believe

there is significant risk of loss in the event of

non-performance by the counterparties associated with

these instruments because these transactions are executed

with a diversified group of major financial institutions.

Further, our policy is to deal with counterparties having a

minimum investment-grade or better credit rating. Credit

risk is managed through the continuous monitoring of

exposures to such counterparties.

Some of our derivative and other material contracts

at December 31, 2006 require us to post cash collateral or

maintain minimum cash balances in escrow. These cash

amounts are reported in our Consolidated Balance Sheets

within Other current assets or Other long-term assets,

depending on when the cash will be contractually

released, as presented in Note 1-Summary of Significant

Accounting Policies to the Consolidated Financial

Statements.

Interest Rate Risk Management: We use interest

rate swap agreements to manage our interest rate

exposure and to achieve a desired proportion of variable

and fixed rate debt. These derivatives may be designated

as fair value hedges or cash flow hedges depending on the

nature of the risk being hedged. Virtually all customer-

financing assets earn fixed rates of interest and a portion

of those assets have been matched to secured borrowings

through third party funding arrangements which generally

bear fixed rates of interest. These borrowings are secured

by customer-financing assets and are designed to mature

as we collect principal payments on the financing assets

which secure them. The interest rates on a significant

portion of those loans are fixed. As a result, these funding

arrangements create natural match funding of the

financing assets to the related debt.

At December 31, 2006 and 2005, we had outstanding

single currency interest rate swap agreements with

aggregate notional amounts of $1.7 billion and $2.1

billion, respectively. The net liability fair values at

December 31, 2006 and 2005 were $41 and $40,

respectively.

81