Xerox 2006 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2006 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

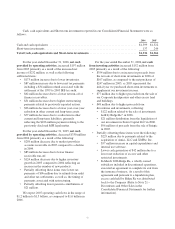

The following table summarizes our secured and

unsecured debt as of December 31, 2006 and 2005:

(in millions) 2006 2005

Term Loan ...................... $ — $ 300

Debt secured by finance

receivables .................... 2,059 2,982

Capital leases .................... 28 38

Debt secured by other assets ........ — 213

Total Secured Debt ........... 2,087 3,533

Senior Notes ..................... 4,224 2,862

Subordinated debt ................ 19 19

Other Debt ...................... 815 864

Total Unsecured Debt ......... 5,058 3,745

Total Debt $7,145 $7,278

At December 31, 2006, approximately 29% of total

debt was secured by finance receivables and other assets

compared to 49% at December 31, 2005. Consistent with

our objective to rebalance the ratio of secured and unsecured

debt, we expect payments on secured loans will continue to

exceed proceeds from new secured loans in 2007.

Credit Facility: In April 2006, we entered into a

$1.25 billion unsecured revolving credit facility including

a $200 million letter of credit subfacility (the “2006

Credit Facility” or “facility”). The facility allows us to

increase from time to time, with willing lenders, the

overall size of the 2006 Credit Facility to an aggregate

amount not to exceed $2 billion. The facility is available,

without sublimit, to certain of our qualifying subsidiaries.

The facility replaces our 2003 Credit Facility that was

terminated upon effectiveness of the 2006 Credit Facility.

As of December 31, 2006, we had outstanding letters of

credit of $15 million and no borrowings under the 2006

Credit Facility. In conjunction with the 2006 Credit

Facility, debt issuance costs of $5 million were deferred.

In connection with the effectiveness of the 2006

Credit Facility, we terminated the 2003 Credit Facility in

April 2006 and repaid all advances outstanding

thereunder, including a $300 million secured term loan,

with a combination of cash on hand and proceeds from

the capital markets offerings. The termination of the 2003

Credit Facility resulted in the second quarter 2006

write-off of the remaining unamortized deferred debt

issuance costs of $13 million ($9 million after-tax).

Refer to Note 11 – Debt to the Consolidated

Financial Statements for further information regarding

our 2006 Credit Facility.

Liquidity, Financial Flexibility and

Other Financing Activity:

Liquidity: We manage our worldwide liquidity

using internal cash management practices, which are

subject to (1) the statutes, regulations and practices of

each of the local jurisdictions in which we operate,

(2) the legal requirements of the agreements to which we

are a party and (3) the policies and cooperation of the

financial institutions we utilize to maintain and provide

cash management services.

As of December 31, 2006, we had $1.5 billion of

cash, cash equivalents and short-term investments, and

borrowing capacity under our 2006 Credit Facility of

approximately $1.235 billion. Our ability to maintain

positive liquidity going forward depends on our ability to

continue to generate cash from operations and access the

financial markets, both of which are subject to general

economic, financial, competitive, legislative, regulatory

and other market factors that are beyond our control.

Share Repurchase Programs: The board of

directors has authorized programs for the repurchase of

the Company’s common stock totaling $2.0 billion as of

December 31, 2006. Since launching our stock buyback

program in October 2005, we have repurchased

100.6 million shares, totaling approximately $1.5 billion

of the $2.0 billion authorized.

Refer to Note 18 – Common Stock and Note 22 –

Subsequent Event in the Consolidated Financial

Statements for further information regarding our share

repurchase programs.

Loan Covenants and Compliance: At December 31,

2006, we were in full compliance with the covenants and

other provisions of the 2006 Credit Facility, the senior

notes and the Loan Agreement. Any failure to be in

compliance with any material provision or covenant of the

2006 Credit Facility or the senior notes could have a

material adverse effect on our liquidity and operations.

Failure to be in compliance with the covenants in the Loan

Agreement, including the financial maintenance covenants

incorporated from the 2006 Credit Facility, would result in

an event of termination under the Loan Agreement and in

such case General Electric Capital Corporation (“GECC”)

would not be required to make further loans to us. If

GECC were to make no further loans to us and assuming a

similar facility was not established and that we were

unable to obtain replacement financing in the public debt

markets, it could materially adversely affect our liquidity

and our ability to fund our customers’ purchases of our

equipment and this could materially adversely affect our

results of operations. We have the right at any time to

45