Target 2012 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2012 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

Forward-Looking Statements

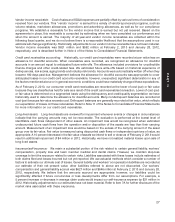

This report contains forward-looking statements, which are based on our current assumptions and expectations.

These statements are typically accompanied by the words ‘‘expect,’’ ‘‘may,’’ ‘‘could,’’ ‘‘believe,’’ ‘‘would,’’ ‘‘might,’’

‘‘anticipates,’’ or words of similar import. The principal forward-looking statements in this report include: For our

U.S. Credit Card Segment, aggregate portfolio risks; for our Canadian Segment, the timing and amount of future

capital investments in Canada and our subsequent financial performance; on a consolidated basis, statements

regarding the adequacy of and costs associated with our sources of liquidity, the fair value of our consumer credit

card receivables, the pending sale of these receivables and related gain, including beneficial interest, the

application of proceeds from the sale and the impact on our future results of operations, earnings and rates, the

continued execution of our share repurchase program, our expected capital expenditures, the expected effective

income tax rate, the expected compliance with debt covenants, the expected impact of new accounting

pronouncements, our intentions regarding future dividends, contributions and payments related to our pension

and postretirement health care plans, the expected returns on pension plan assets, the impact of future changes in

foreign currency exchange rates, the expected changes in gross margin and SG&A rates, the effects of

macroeconomic conditions, the adequacy of our reserves for general liability, workers’ compensation and property

loss, the expected outcome of claims and litigation, the expected ability to recognize deferred tax assets and

liabilities, including foreign net operating loss carryforwards, and the resolution of tax matters.

All such forward-looking statements are intended to enjoy the protection of the safe harbor for forward-looking

statements contained in the Private Securities Litigation Reform Act of 1995, as amended. Although we believe

there is a reasonable basis for the forward-looking statements, our actual results could be materially different. The

most important factors which could cause our actual results to differ from our forward-looking statements are set

forth on our description of risk factors in Item 1A to this Form 10-K, which should be read in conjunction with the

forward-looking statements in this report. Forward-looking statements speak only as of the date they are made, and

we do not undertake any obligation to update any forward-looking statement.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

At February 2, 2013, our exposure to market risk was primarily from interest rate changes on our debt obligations,

some of which are at a LIBOR-plus floating-rate, and on our credit card receivables, the majority of which are

assessed finance charges at a Prime-based floating-rate. Historically, to manage our net interest margin, we

generally maintained levels of floating-rate debt to generate similar changes in net interest expense as finance

charge revenues fluctuated. The degree of floating asset and liability matching varied over time and in different

interest rate environments. At February 2, 2013, the amount of floating-rate credit card assets exceeded the amount

of net floating-rate debt obligations by approximately $1 billion. See further description of our debt and derivative

instruments in Notes 20 and 21 of the Notes to Consolidated Financial Statements. As a result of the sale of our

consumer credit card portfolio, funding risk was transferred to TD Bank Group. Following the sale, our interest rate

exposure will primarily be due to the extent by which our floating rate debt obligations differ from our floating rate

short term investments. In general, we expect our floating rate debt to exceed our floating rate short term

investments over time but that may vary in different interest rate environments.

We record our general liability and workers’ compensation liabilities at net present value; therefore, these liabilities

fluctuate with changes in interest rates. Periodically, in certain interest rate environments, we economically hedge a

portion of our exposure to these interest rate changes by entering into interest rate forward contracts that partially

mitigate the effects of interest rate changes. Based on our balance sheet position at February 2, 2013, the

annualized effect of a 0.5 percentage point decrease in interest rates would be to decrease earnings before income

taxes by $9 million.

In addition, we are exposed to market return fluctuations on our qualified defined benefit pension plans. A

0.5 percentage point decrease to the weighted average discount rate would increase annual expense by

$28 million. The value of our pension liabilities is inversely related to changes in interest rates. To protect against

29

PART II