Pizza Hut 2012 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2012 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

YUM! BRANDS, INC.-2012 Form10-K 45

Form 10-K

PART II

ITEM 8Financial Statements andSupplementaryData

costs which will generally be used for the fi rst time in the next fi scal year

and have historically not been signifi cant.To the extent we participate in

advertising cooperatives, we expense our contributions as incurred which

are generally based on a percentage of sales.Our advertising expenses

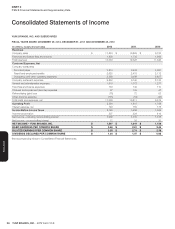

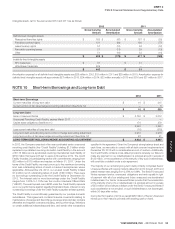

were $608million, $593million and $557million in 2012, 2011 and 2010,

respectively.We report substantially all of our direct marketing costs in

Occupancy and other operating expenses.

Research and Development Expenses.Research and development

expenses, which we expense as incurred, are reported in G&A

expenses.Research and development expenses were $30million, $34million

and $33million in 2012, 2011 and 2010, respectively.

Share-Based Employee Compensation.We recognize all share-based

payments to employees, including grants of employee stock options

and stock appreciation rights (“SARs”), in the Consolidated Financial

Statements as compensation cost over the service period based on their

fair value on the date of grant.This compensation cost is recognized over

the service period on a straight-line basis for the fair value of awards that

actually vest.We present this compensation cost consistent with the

other compensation costs for the employee recipient in either Payroll and

employee benefi ts or G&A expenses.

Legal Costs. Settlement costs are accrued when they are deemed

probable and estimable. Anticipated legal fees related to self-insured

workers’ compensation, employment practices liability, general liability,

automobile liability, product liability and property losses (collectively,

“property and casualty losses”) are accrued when deemed probable and

estimable. Legal fees not related to self-insured property and casualty

losses are recognized as incurred.

Impairment or Disposal of Property, Plant and Equipment.Property,

plant and equipment (“PP&E”) is tested for impairment whenever events

or changes in circumstances indicate that the carrying value of the assets

may not be recoverable.The assets are not recoverable if their carrying

value is less than the undiscounted cash fl ows we expect to generate from

such assets.If the assets are not deemed to be recoverable, impairment is

measured based on the excess of their carrying value over their fair value.

For purposes of impairment testing for our restaurants, we have concluded

that an individual restaurant is the lowest level of independent cash fl ows

unless our intent is to refranchise restaurants as a group.We review our

long-lived assets of such individual restaurants (primarily PP&E and allocated

intangible assets subject to amortization) semi-annually for impairment, or

whenever events or changes in circumstances indicate that the carrying

amount of a restaurant may not be recoverable.We use two consecutive

years of operating losses as our primary indicator of potential impairment

for our semi-annual impairment testing of these restaurant assets.We

evaluate the recoverability of these restaurant assets by comparing the

estimated undiscounted future cash fl ows, which are based on our entity-

specifi c assumptions, to the carrying value of such assets.For restaurant

assets that are not deemed to be recoverable, we write-down an impaired

restaurant to its estimated fair value, which becomes its new cost basis.Fair

value is an estimate of the price a franchisee would pay for the restaurant

and its related assets and is determined by discounting the estimated

future after-tax cash fl ows of the restaurant, which include a deduction

we would receive under a franchise agreement with terms substantially

at market.The after-tax cash fl ows incorporate reasonable assumptions

we believe a franchisee would make such as sales growth and margin

improvement.The discount rate used in the fair value calculation is our

estimate of the required rate of return that a franchisee would expect to

receive when purchasing a similar restaurant and the related long-lived

assets.The discount rate incorporates rates of returns for historical

refranchising market transactions and is commensurate with the risks

and uncertainty inherent in the forecasted cash fl ows.

In executing our refranchising initiatives, we most often offer groups of

restaurants for sale.When we believe a restaurant or groups of restaurants

will be refranchised for a price less than their carrying value, but do not

believe the restaurant(s) have met the criteria to be classifi ed as held for sale,

we review the restaurants for impairment.We evaluate the recoverability

of these restaurant assets at the date it is considered more likely than not

that they will be refranchised by comparing estimated sales proceeds plus

holding period cash fl ows, if any, to the carrying value of the restaurant

or group of restaurants.For restaurant assets that are not deemed to be

recoverable, we recognize impairment for any excess of carrying value

over the fair value of the restaurants, which is based on the expected net

sales proceeds.To the extent ongoing agreements to be entered into with

the franchisee simultaneous with the refranchising are expected to contain

terms, such as royalty rates, not at prevailing market rates, we consider

the off-market terms in our impairment evaluation.We recognize any such

impairment charges in Refranchising (gain) loss.We classify restaurants

as held for sale and suspend depreciation and amortization when (a) we

make a decision to refranchise; (b) the restaurants can be immediately

removed from operations; (c) we have begun an active program to locate a

buyer; (d) the restaurant is being actively marketed at a reasonable market

price; (e) signifi cant changes to the plan of sale are not likely; and (f) the

sale is probable within one year.Restaurants classifi ed as held for sale

are recorded at the lower of their carrying value or fair value less cost to

sell.We recognize estimated losses on restaurants that are classifi ed as

held for sale in Refranchising (gain) loss.

Refranchising (gain) loss includes the gains or losses from the sales of

our restaurants to new and existing franchisees, including impairment

charges discussed above, and the related initial franchise fees. We

recognize gains on restaurant refranchisings when the sale transaction

closes, the franchisee has a minimum amount of the purchase price in

at-risk equity, and we are satisfi ed that the franchisee can meet its fi nancial

obligations.If the criteria for gain recognition are not met, we defer the

gain to the extent we have a remaining fi nancial exposure in connection

with the sales transaction.Deferred gains are recognized when the gain

recognition criteria are met or as our fi nancial exposure is reduced.When

we make a decision to retain a store, or group of stores, previously held

for sale, we revalue the store at the lower of its (a) net book value at our

original sale decision date less normal depreciation and amortization that

would have been recorded during the period held for sale or (b) its current

fair value.This value becomes the store’s new cost basis.We record any

resulting difference between the store’s carrying amount and its new cost

basis to Closure and impairment (income) expense.

When we decide to close a restaurant, it is reviewed for impairment and

depreciable lives are adjusted based on the expected disposal date.Other

costs incurred when closing a restaurant such as costs of disposing of the

assets as well as other facility-related expenses from previously closed

stores are generally expensed as incurred.Additionally, at the date we

cease using a property under an operating lease, we record a liability for

the net present value of any remaining lease obligations, net of estimated

sublease income, if any.Any costs recorded upon store closure as well as

any subsequent adjustments to liabilities for remaining lease obligations as

a result of lease termination or changes in estimates of sublease income

are recorded in Closures and impairment (income) expenses.To the

extent we sell assets, primarily land, associated with a closed store, any

gain or loss upon that sale is also recorded in Closures and impairment

(income) expenses.

Considerable management judgment is necessary to estimate future cash

fl ows, including cash fl ows from continuing use, terminal value, sublease

income and refranchising proceeds.Accordingly, actual results could vary

signifi cantly from our estimates.

Impairment of Investments in Unconsolidated Affi liates.We record

impairment charges related to an investment in an unconsolidated affi liate

whenever events or circumstances indicate that a decrease in the fair value

of an investment has occurred which is other than temporary.In addition,

we evaluate our investments in unconsolidated affi liates for impairment

when they have experienced two consecutive years of operating losses.We

recorded no impairment associated with our investments in unconsolidated

affi liates during 2012, 2011 and 2010.

Guarantees.We recognize, at inception of a guarantee, a liability for the fair

value of certain obligations undertaken.The majority of our guarantees are

issued as a result of assigning our interest in obligations under operating