Pep Boys 2011 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2011 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 29, 2011, January 30, 2010 and January 31, 2009

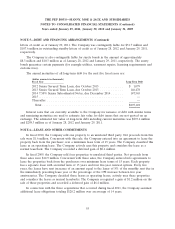

NOTE 5—DEBT AND FINANCING ARRANGEMENTS (Continued)

Senior Secured Term Loan Facility, due October 2013

The Company has a Senior Secured Term Loan facility (the ‘‘Term Loan’’) due October 2013. This

facility is secured by a collateral pool consisting of real property and improvements associated with

stores, which is adjusted periodically based upon real estate values and borrowing levels. Interest

accrues at the three month London Interbank Offered Rate (LIBOR) plus 2.0% on this facility. As of

January 28, 2012, 126 stores collateralized the Term Loan.

Revolving Credit Agreement, through July 2016

On January 16, 2009, the Company entered into a Revolving Credit Agreement (the ‘‘Agreement’’)

with available borrowings up to $300.0 million and a maturity of January 2014. Total incurred fees of

$6.8 million were capitalized and are being amortized over the original five year life of the facility. On

July 26, 2011, the Company amended and restated the Agreement to reduce its interest rate by 75 basis

points and to extend its maturity to July 2016. The related refinancing fees of $2.4 million are being

amortized over the new five year life. The Company’s ability to borrow under the Agreement is based

on a specific borrowing base consisting of inventory and accounts receivable. The interest rate on this

credit line is daily LIBOR plus 2.00% to 2.50% based upon the then current availability under the

Agreement. Fees based on the unused portion of the Agreement range from 37.5 to 75.0 basis points.

As of January 28, 2012, there were no outstanding borrowings under the Agreement.

The weighted average interest rate on all debt borrowings during fiscal 2011 and 2010 was 6.3%.

Other Matters

Several of the Company’s debt agreements require compliance with covenants. The most restrictive

of these covenants, an earnings before interest, taxes, depreciation and amortization (‘‘EBITDA’’)

requirement, is triggered if the Company’s availability under its credit agreement drops below

$50.0 million. The failure to satisfy this covenant would constitute an event of default under the

Revolving Credit Agreement, which would result in a cross-default under the Notes and Term Loan.

As of January 28, 2012, the Company had no borrowings outstanding under the Revolving Credit

Agreement, additional availability of approximately $194.9 million and was in compliance with all

financial covenants contained in its debt agreements.

Other Contractual Obligations

The Company has a vendor financing program with availability up to $125.0 million which is

funded by various bank participants who have the ability, but not the obligation, to purchase account

receivables owed by the Company directly from vendors. The Company, in turn, makes the regularly

scheduled full vendor payments to the bank participants. There was an outstanding balance of

$85.2 million and $56.3 million under the program as of January 28, 2012 and January 29, 2011,

respectively.

The Company has letter of credit arrangements in connection with its risk management, import

merchandising and vendor financing programs. The Company had no outstanding commercial letters of

credit as of January 28, 2012 and was contingently liable for $0.3 million in outstanding commercial

54