Metro PCS 2007 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2007 Metro PCS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

55

million and an immaterial amount of state income tax during the years ended December 31, 2007 and 2006,

respectively.

Seasonality

Our customer activity is influenced by seasonal effects related to traditional retail selling periods and other factors

that arise from our target customer base. Based on historical results, we generally expect net customer additions to

be strongest in the first and fourth quarters. Softening of sales and increased customer turnover, or churn, in the

second and third quarters of the year usually combine to result in fewer net customer additions. However, sales

activity and churn can be strongly affected by the launch of new markets and promotional activity, which have the

ability to reduce or outweigh certain seasonal effects.

Net Additions

Subscribers

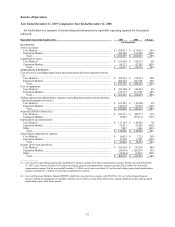

MetroPCS Subscriber Statistics

Core

Markets

Expansion

Markets

Consolidated

Core

Markets

Expansion

Markets

Consolidated

(In 000s)

2004

Q1............................................................ 174 — 174 1,151 — 1,151

Q2............................................................ 63 — 63 1,214 — 1,214

Q3............................................................ 66 — 66 1,280 — 1,280

Q4............................................................ 119 — 119 1,399 — 1,399

2005

Q1............................................................ 169 — 169 1,568 — 1,568

Q2............................................................ 77 — 77 1,645 — 1,645

Q3............................................................ 95 — 95 1,740 — 1,740

Q4............................................................ 132 53 185 1,872 53 1,925

2006

Q1............................................................ 184 61 245 2,056 114 2,170

Q2............................................................ 63 186 249 2,119 300 2,419

Q3............................................................ 55 142 198 2,174 442 2,617

Q4............................................................ 127 198 324 2,301 640 2,941

2007

Q1............................................................ 184 270 454 2,485 910 3,395

Q2............................................................ 58 97 155 2,543 1,007 3,550

Q3............................................................ 36 78 114 2,578 1,086 3,664

Q4............................................................ 81 218 299 2,659 1,304 3,963

Operating Segments

Operating segments are defined by SFAS No. 131 “Disclosure About Segments of an Enterprise and Related

Information,” (“SFAS No. 131”), as components of an enterprise about which separate financial information is

available that is evaluated regularly by the chief operating decision maker in deciding how to allocate resources and

in assessing performance. Our chief operating decision maker is the Chairman of the Board, Chief Executive Officer

and President.

As of December 31, 2007, we had twelve operating segments based on geographic region within the United

States: Atlanta, Boston, Dallas/Ft. Worth, Detroit, Las Vegas, Los Angeles, Miami, New York, Philadelphia,

San Francisco, Sacramento and Tampa/Sarasota/Orlando. Each of these operating segments provide wireless voice

and data services and products to customers in its service areas or is currently constructing a network in order to

provide these services. These services include unlimited local and long distance calling, voicemail, caller ID, call

waiting, enhanced directory assistance, text messaging, picture and multimedia messaging, international long

distance and international text messaging, ringtones, games and content applications, unlimited directory assistance,

ring back tones, nationwide roaming, mobile Internet browsing, mobile instant messaging, push e-mail and other

value-added services.

We aggregate our operating segments into two reportable segments: Core Markets and Expansion Markets.

• Core Markets, which include Atlanta, Miami, San Francisco, and Sacramento, are aggregated because they

are reviewed on an aggregate basis by the chief operating decision maker, they are similar in respect to their

products and services, production processes, class of customer, method of distribution, and regulatory

environment and currently exhibit similar financial performance and economic characteristics.