MasterCard 2012 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2012 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Refunding Revenue Bonds

The Company holds refunding revenue bonds with the same payment terms, and which contain the right of

set-off with a capital lease obligation related to the Company’s global technology and operations center located

in O’Fallon, Missouri. The Company has netted the refunding revenue bonds and the corresponding capital lease

obligation in the consolidated balance sheet and estimates that the carrying value approximates the fair value for

these bonds. See Note 7 (Property, Plant and Equipment) for further details.

Non-Financial Instruments

Certain assets and liabilities are measured at fair value on a nonrecurring basis for purposes of initial

recognition and impairment testing. The Company’s non-financial assets and liabilities measured at fair value on

a nonrecurring basis include property, plant and equipment, goodwill and other intangible assets. These assets are

not measured at fair value on an ongoing basis; however, they are subject to fair value adjustments in certain

circumstances, such as when there is evidence of impairment.

The valuation methods for goodwill and other intangible assets involve assumptions concerning comparable

company multiples, discount rates, growth projections and other assumptions of future business conditions. The

Company uses a weighted income and market approach for estimating the fair value of its reporting unit, when

necessary. As the assumptions employed to measure these assets on a nonrecurring basis are based on

management’s judgment using internal and external data, these fair value determinations are classified in Level 3

of the Valuation Hierarchy.

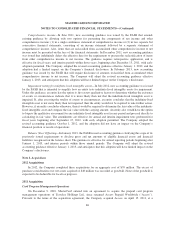

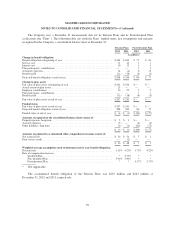

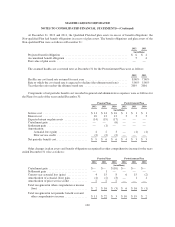

Amortized Costs and Fair Values—Available-for-Sale Investment Securities

The major classes of the Company’s available-for-sale investment securities, for which unrealized gains and

losses are recorded as a separate component of other comprehensive income on the consolidated statement of

comprehensive income, and their respective amortized cost basis and fair values as of December 31, 2012 and

2011 were as follows:

December 31, 2012

Amortized

Cost

Gross

Unrealized

Gain

Gross

Unrealized

Loss1

Fair

Value

(in millions)

Municipal securities ........................... $ 522 $ 9 $— $ 531

U.S. Government and Agency securities ........... 582 — — 582

Taxable short-term bond funds .................. 209 1 — 210

Corporate securities ........................... 1,245 2 (1) 1,246

Asset-backed securities ........................ 316 — — 316

Auction rate securities2........................ 35 — (3) 32

Other ...................................... 66 — — 66

Total ....................................... $2,975 $ 12 $ (4) $2,983

92