MasterCard 2012 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2012 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

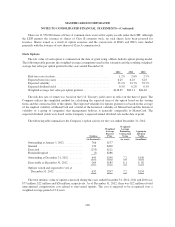

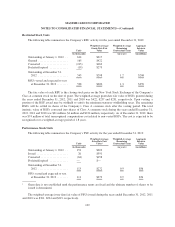

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

an adverse outcome in a regulatory proceeding could lead to the filing of civil damage claims and possibly result

in damage awards in amounts that could be significant. Any of these events could have a material adverse effect

on MasterCard’s results of operations, financial condition and overall business.

Department of Justice Antitrust Litigation and Related Private Litigations

In October 1998, the U.S. Department of Justice (“DOJ”) filed suit against MasterCard International, Visa

U.S.A., Inc. and Visa International Corp. in the U.S. District Court for the Southern District of New York

alleging that both MasterCard’s and Visa’s governance structure and policies violated U.S. federal antitrust laws.

The DOJ challenged (1) “dual governance”, where a financial institution has a representative on the Board of

Directors of MasterCard or Visa while a portion of its card portfolio is issued under the brand of the other

association, and (2) both MasterCard’s Competitive Programs Policy (“CPP”) and a Visa bylaw provision that

prohibited financial institutions participating in the respective associations from issuing competing proprietary

payment cards (such as American Express or Discover). In October 2001, the judge issued an opinion upholding

the legality and pro-competitive nature of dual governance. However, the judge also held that MasterCard’s CPP

and the Visa bylaw constituted unlawful restraints of trade under the federal antitrust laws. The judge

subsequently issued a final judgment that ordered MasterCard to repeal the CPP and enjoined MasterCard from

enacting or enforcing any bylaw, rule, policy or practice that prohibits its issuers from issuing general purpose

credit or debit cards in the United States on any other general purpose card network.

In April 2005, a complaint was filed in California state court on behalf of a putative class of consumers

under California unfair competition law (Section 17200) and the Cartwright Act (the “Attridge action”). The

claims in this action seek to piggyback on the portion of the DOJ antitrust litigation discussed above with regard

to the District Court’s findings concerning MasterCard’s CPP and Visa’s related bylaw. The Court granted the

defendants’ motion to dismiss the plaintiffs’ Cartwright Act claims but denied the defendants’ motion to dismiss

the plaintiffs’ Section 17200 unfair competition claims. The parties have proceeded with discovery. In September

2009, MasterCard executed a settlement agreement that is subject to court approval in the separate California

consumer litigations (see “U.S. Merchant and Consumer Litigations”). The agreement includes a release that the

parties believe encompasses the claims asserted in the Attridge action. In August 2010, the Court in the

California consumer actions granted final approval to the settlement. The plaintiff from the Attridge action and

three other objectors filed appeals of the settlement approval. In January 2012, the Appellate Court reversed the

trial court’s settlement approval and remanded the matter to the trial court for further proceedings. In August

2012, the parties in the California consumer actions filed a motion seeking approval of a revised settlement

agreement. In November 2012, the trial court granted preliminary approval of the settlement and scheduled a

hearing on the final approval of the settlement for April 2013.

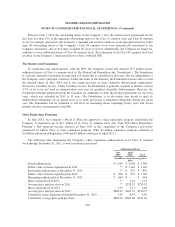

U.S. Merchant and Consumer Litigations

Commencing in October 1996, several class action suits were brought by a number of U.S. merchants

against MasterCard International and Visa U.S.A., Inc. challenging certain aspects of the payment card industry

under U.S. federal antitrust law. The plaintiffs claimed that MasterCard’s “Honor All Cards” rule (and a similar

Visa rule), which required merchants who accept MasterCard cards to accept for payment every validly presented

MasterCard card, constituted an illegal tying arrangement in violation of Section 1 of the Sherman Act. In June

2003, MasterCard International signed a settlement agreement to settle the claims brought by the plaintiffs in this

matter, which the Court approved in December 2003. Pursuant to the settlement, MasterCard agreed, among

other things, to create two separate “Honor All Cards” rules in the United States—one for debit cards and one for

credit cards.

115