MasterCard 2012 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2012 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

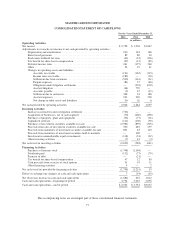

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Business combinations—The Company accounts for businesses acquired in business combinations under the

acquisition method of accounting. The Company measures the tangible and intangible identifiable assets

acquired, liabilities assumed, and any noncontrolling interest in the acquiree at the acquisition date, at their fair

values as of that date. Acquisition-related costs are expensed separately from the business combination and are

included in general and administrative expenses. Any excess of purchase price over the fair value of net assets

acquired, including identifiable intangible assets, is recorded as goodwill. See Note 8 (Goodwill) for additional

information on the Company’s goodwill.

Intangible assets—Intangible assets consist of capitalized software costs, trademarks, tradenames, customer

relationships and other intangible assets, which have finite lives, and customer relationships which have

indefinite lives. Intangible assets with finite useful lives are amortized over their estimated useful lives, which

range from one to ten years, under the straight-line method. Capitalized software includes internal costs incurred

for payroll and payroll related expenses directly related to the design, development and testing phases of each

capitalized software project.

Impairment of assets—Long-lived assets, other than goodwill and indefinite-lived intangible assets, are

tested for impairment whenever events or circumstances indicate that their carrying amount may not be

recoverable. If the carrying value of the asset cannot be recovered from estimated future cash flows,

undiscounted and without interest, the fair value of the asset is calculated using the present value of estimated net

future cash flows. If the carrying amount of the asset exceeds its fair value, an impairment is recorded. The

Company regularly reviews investments accounted for under the cost and equity methods for possible

impairment, which generally involves an analysis of the facts and circumstances influencing the investment,

expectations of the entity’s cash flows and capital needs, and the viability of the business model.

Goodwill and indefinite-lived intangible assets are tested annually for impairment in the fourth quarter, or

sooner when circumstances indicate an impairment may exist, using a qualitative analysis. The impairment

evaluation utilizes a qualitative assessment to determine whether it is more likely than not (that is, a likelihood of

more than 50 percent) that the fair value of the reporting unit or indefinite-lived intangible asset is less than its

carrying amount and whether it is necessary to perform a quantitative impairment test. If, after performing a

qualitative assessment, it is determined that it is more likely than not that the fair value of the reporting unit or

indefinite-lived intangible asset is less than its carrying amount, then it would be necessary to use the quantitative

impairment test to identify potential impairment and measure the amount of an impairment loss to be recognized

(if any). The quantitative impairment test is not necessary if, after performing the qualitative assessment, it is

determined that it is more likely than not that the fair value of the reporting unit or indefinite-lived intangible

assets exceeds its carrying amount. Impairment charges, if any, are recorded in general and administrative

expenses. A reporting unit is the operating segment, or a business, which is one level below that operating

segment (the “component” level) if discrete financial information is prepared and regularly reviewed by

management at the segment level. Components are aggregated as a single reporting unit if they have similar

economic characteristics.

Litigation—The Company is a party to certain legal and regulatory proceedings with respect to a variety of

matters. Except as described in Note 18 (Legal and Regulatory Proceedings), MasterCard does not believe that

any legal or regulatory proceedings to which it is a party would have a material adverse impact on its business or

prospects. The Company evaluates the likelihood of an unfavorable outcome of all legal or regulatory

proceedings to which it is a party and accrues a loss contingency when the loss is probable and reasonably

estimable. These judgments are subjective based on the status of the legal or regulatory proceedings, the merits

of its defenses and consultation with in-house and external legal counsel. The actual outcomes of these

proceedings may materially differ from the Company’s judgments. Legal costs are expensed as incurred and

recorded in general and administrative expenses.

80