MasterCard 2012 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2012 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

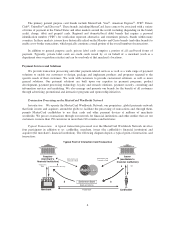

•Cross-Border and Domestic Processing. The MasterCard Worldwide Network provides our customers

with a flexible structure that enables them to support processing across regions and for domestic

markets. The network processes transactions throughout the world on our products where the merchant

country and issuer country are different (cross-border transactions). We process transactions

denominated in more than 150 currencies through our global system, providing cardholders with the

ability to utilize, and merchants to accept, MasterCard cards and other payment devices across multiple

country borders. For example, we may process a transaction in a merchant’s local currency; however,

the charge for the transaction would appear on the cardholder’s statement in the cardholder’s home

currency. We also provide domestic (or intra-country) transaction processing services to customers in

every region of the world, which allow customers to facilitate payment transactions between cardholders

and merchants within a particular country. We process most of the cross-border transactions using

MasterCard, Maestro and Cirrus-branded cards and process the majority of MasterCard-branded

domestic transactions in the United States, United Kingdom, Canada, Brazil and a select number of

other countries. Outside of these countries, most intra-country (as opposed to cross-border) transaction

activity conducted with our payment products is authorized, cleared and/or settled by our customers or

other processors without the involvement of the MasterCard Worldwide Network. We continue to invest

in our network and build relationships to expand opportunities for domestic transaction processing. In

particular, the Single European Payment Area (“SEPA”) initiative creates an open and competitive

market in many European countries that were previously mandated to process domestic debit

transactions with domestic processors. As a result, in addition to cross-border transactions, we now

process some domestic debit transactions in virtually every SEPA country.

•Extended Processing Capabilities. In addition to transaction switching, we continually evaluate and

invest in ways to strategically extend our processing capabilities in the payments value chain by seeking

to provide our customers with an expanded suite of payment processing solutions that meet the unique

processing needs of their markets. Examples include:

OMasterCard Integrated Processing Solutions®.MasterCard Integrated Processing Solutions

(“IPS”) is a debit and prepaid issuer processing platform designed to provide medium to large global

issuing customers with a complete processing solution to help create differentiated products and

services and allow quick deployment of payments portfolios across banking channels. Through a

single processing platform, IPS can, among other things, authorize debit and prepaid transactions,

assist issuers in managing risk using fraud detection tools, manage an issuer’s card base, and

manage and monitor an issuer’s ATMs. The proprietary MasterCard Total Portfolio View™ tool

provides a user-friendly customer interface to IPS, delivering aggregate cardholder intelligence

across accounts and product lines to provide our customers with a view of information that can help

them customize their products and programs. We continue to develop opportunities to further

enhance our IPS offerings and global presence.

OInternet Payment Gateways. We provide e-commerce processing solutions through internet

payment gateways, which are interfaces between merchants and acquirers that help move a

transaction through the payments network. Our gateways include DataCash®and MasterCard

Internet Gateway Service (MiGS), which offer payment service provider solutions across the globe.

These gateways offer a single interface to provide e-commerce merchants with the ability to process

secure payments and offer value-added solutions, including outsourced electronic payments, fraud

prevention and alternative payment options.

OStrategic Investments. We have invested strategically in various regions around the globe to

pursue opportunities in issuer, prepaid, acquirer and third-party processing. These investments

support and/or provide, among other things, prepaid processing, acquirer processing, third-party

processing services and software (as well as switching solutions) and complete processing solutions

for mobile payments.

9