LensCrafters 2009 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2009 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS | 81 <

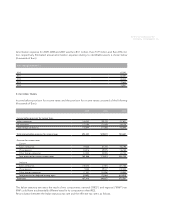

During the fourth quarter of 2008 and the first quarter of 2009, US Holdings entered into 14 interest

rate swap transactions with an aggregate initial notional amount of US$ 700.0 million with various banks

("Tranche D Swaps").The last maturity of these swaps will be October 12, 2012. The Tranche D Swaps

were entered into as a cash flow hedge on Facility D of the credit facility discussed above. The Tranche

D Swaps exchange the floating rate of LIBOR for an average fixed rate of 2.42 percent per annum. The

ineffectiveness of cash flow hedges was tested at the inception date and at least every three months.

The results of the tests indicated that the cash flow hedges are highly effective. As a consequence ap-

proximately US$ (8.0) million, net of taxes, is included in other comprehensive income as of December

31, 2009. Based on current interest rates and market conditions, the estimated aggregate amount to

be recognized in earnings from other comprehensive income for these hedges in fiscal 2010 is approxi-

mately US$ (8.7) million, net of taxes.

The short-term bridge loan facility was for an aggregate principal amount of US$ 500 million. Interest

accrued on the short term bridge loan at LIBOR (as defined in the agreement) plus 0.15 percent. The

final maturity of the credit facility was eight months from the first utilization date. On April 29, 2008,

the Company and its subsidiary US Holdings entered into an amendment and transfer agreement to

the US$ 500.0 million short-term bridge loan facility entered into to finance the Oakley acquisition.

The terms of this amendment and transfer agreement, among other things, reduced the total facility

amount from US$ 500.0 million to US$ 150.0 million, effective on July 1, 2008, and provided for a final

maturity date that is 18 months from the effective date of the agreement. From July 1, 2008, interest ac-

crued at LIBOR (as defined in the agreement) plus 0.60 percent. On November 27, 2009, the Company

and its subsidiary, Luxottica US Holdings Corp., amended the US$ 150 million short-term bridge loan

facility amended on April 29, 2008. The new terms, among other things, reduce the total facility amount

from US$ 150 million to US$ 75 million, effective November 30, 2009, and provide for a two year final

maturity date of November 30, 2011. The new terms also provide for the repayment of US$25 million on

November 30, 2010 and the remaining principal at the final maturity date. From November 30, 2009, in-

terest accrues at LIBOR (as defined in the agreement) plus 1.90 percent (2.157 percent as of December

31, 2009). Under this credit facility, US$ 75 million was borrowed as of December 31, 2009.

The fair value of the long term debt is approximately Euro 2.6 billion as of December 31, 2009. The fair value

of the long term borrowings equals the net present value of the future flows, calculated using the current mar-

ket rate available for similar debt facilities, adjusted to take into account the Company’s credit worthiness.

The financial and operating covenants included in the above long term debt include the following:

1. Consolidated Total Net Debt shall not be equal to or exceed 3.5 times the Consolidated EBITDA

2. Consolidated EBITDA shall not be less than five times the Consolidated Net Finance Charges.

Total Net Debt, EBITDA and Net Financial charges are all defined terms of the various credit agreements.

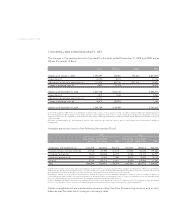

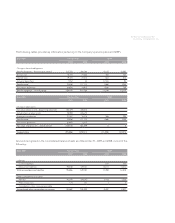

Long-term debt, including capital lease obligations, matures in the years subsequent to December 31,

2009 as follows (thousands of Euro):

Year ended December 31

2010 166,279

2011 282,161

2012 799,398

2013 1,144,450

2014 256

Thereafter 177,925

Total 2,570,469