Lenovo 2011 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2011 Lenovo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

2010/11 Annual Report Lenovo Group Limited 97

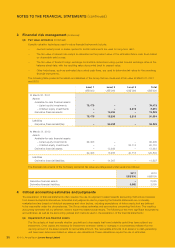

4 Critical accounting estimates and judgments (continued)

(a) Impairment of non-financial assets (continued)

The value-in-use calculations primarily use cash flow projections based on financial budgets, in general covered five

years, approved by management and estimated terminal values at the end of the five-year period. There are a number of

assumptions and estimates involved for the preparation of cash flow projections for the period covered by the approved

budget and the estimated terminal value. Key assumptions include the expected growth in revenues and operating

margin, effective tax rate, growth rates and selection of discount rates, to reflect the risks involved and the earnings

multiple that can be realized for the estimated terminal value.

Management prepared the financial budgets reflecting actual and prior year performance and market development

expectations. Judgment is required to determine key assumptions adopted in the cash flow projections and changes to

key assumptions can significantly affect these cash flow projections and therefore the results of the impairment reviews.

(b) Income taxes

The Group is subject to income taxes in numerous jurisdictions. Significant judgment is required in determining

the worldwide provision for income taxes. There are certain transactions and calculations for which the ultimate

tax determination is uncertain during the ordinary course of business. The tax liabilities recognized are based on

management’s assessment of the likely outcome.

The Group recognizes liabilities for anticipated tax audit issues based on estimates of whether additional taxes will be

due.

Deferred income tax is provided in full, using the liability method, on temporary differences arising between the tax

bases of assets and liabilities and their carrying values in the financial statements.

Deferred income tax assets are mainly recognized for temporary differences such as warranty provision, accrued

sales rebates, bonus accruals, and other accrued expenses, and unused tax losses carried forward to the extent it is

probable that future taxable profits will be available against which deductible temporary differences and the unused

tax losses can be utilized, based on all available evidence. Recognition primarily involves judgment regarding the

future financial performance of the particular legal entity or tax group in which the deferred income tax asset has been

recognized. A variety of other factors are also evaluated in considering whether there is convincing evidence that it is

probable that some portion or all of the deferred income tax assets will ultimately be realized, such as the existence of

taxable temporary differences, group relief, tax planning strategies and the periods in which estimated tax losses can

be utilized. The carrying amount of deferred income tax assets and related financial models and budgets are reviewed

at each balance sheet date and to the extent that there is insufficient convincing evidence that sufficient taxable profits

will be available within the utilization periods to allow utilization of the carry forward tax losses, the asset balance will be

reduced and the difference charged to the income statement.

Where the final tax outcome of these matters is different from the amounts that were initially recorded, such differences

will impact the income tax provisions and deferred income tax assets and liabilities in the period in which such

determination is made.

(c) Warranty provision

Warranty provision is based on the estimated cost of product warranties when revenue is recognized. Factors that affect

the Group’s warranty liability include the number of sold units currently under warranty, historical and anticipated rates

of warranty claims on those units, and cost per claim to satisfy our warranty obligation. The estimation basis is reviewed

on an on-going basis and revised where appropriate. Certain of these costs are reimbursable from the suppliers in

accordance with the terms of relevant arrangement with the suppliers. These amounts are recognized as a separate

asset, to the extent of the amount of the provision made, when it is virtually certain that reimbursement will be received

if the Group settles the obligation.

(d) Revenue recognition

Application of various accounting principles related to the measurement and recognition of revenue requires the Group

to make judgments and estimates. Specifically, complex arrangements with non-standard terms and conditions may

require significant contract interpretation to determine the appropriate accounting, including whether the deliverables

specified in a multiple element arrangement should be treated as separate units of accounting. Other significant

judgments include determining whether the Group or a reseller is acting as the principal in a transaction and whether

separate contracts are considered part of one arrangement.